The question is not if you will experience a declined card in your business; it’s when.

All merchants will see a declined credit card at some point, and the reasons can range from minor technical issues to fraud concerns.

Because the occurrence is so frequent, you have to know how to handle declined cards from customers.

In this post, you can find six tips that will help you deal with credit card declines. If you implement them into your business, you won’t have to dread the payment decline messages that pop on your screen.

Jump to section:

Understand Credit Card Decline Codes

Communicate the Credit Card Decline Empathetically

Suggest Alternative Forms of Payment

Mind the Costs of Declined Transactions

Review Your Payment Gateway Fraud Security Settings

Plan for Credit Card Declines Ahead of Time

Understand Credit Card Decline Codes

The starting point of handling declined credit cards is understanding the source of the issue. Familiarizing yourself with the decline codes will help you pinpoint the issue so you can start working on a solution.

Before we get to the specific codes that show up on your screen when a card is declined, let’s see the general causes of card declines.

More than 1 in 5 consumers say that their credit card has been declined at some point.

Even though the leading reason for declined cards was the exceeded card limit (at 32%), fraud protection and technology issues were significant contributors as well.

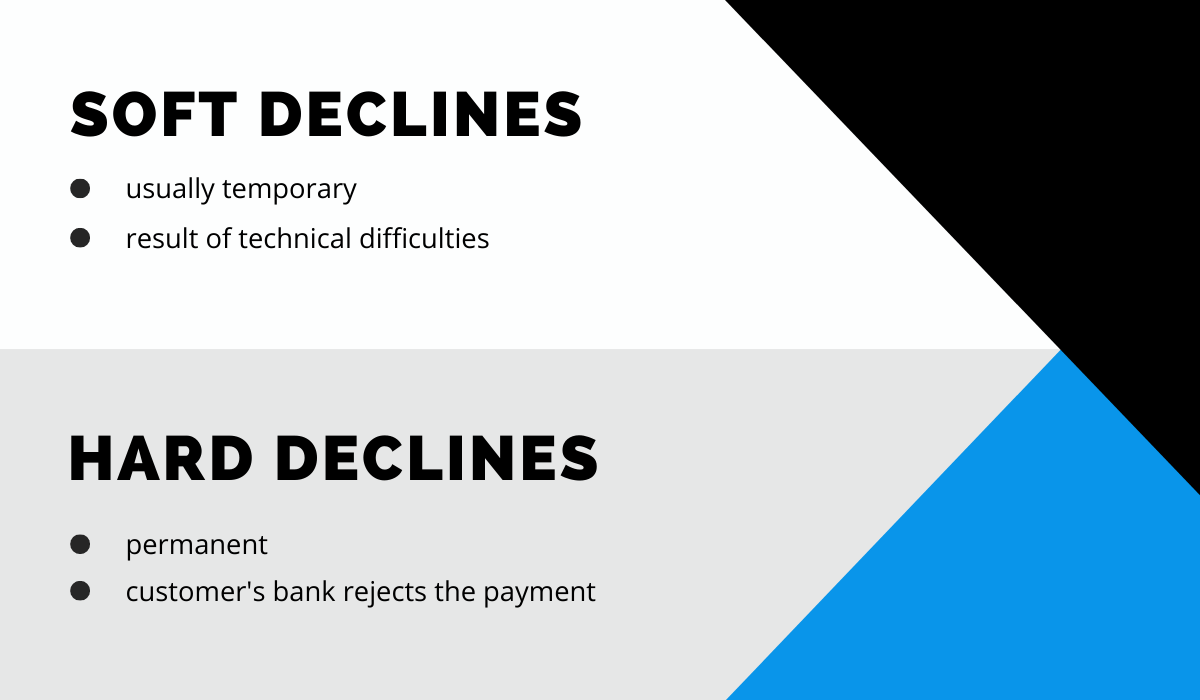

Not all issues are equally severe. A glitch can happen somewhere in the payment processing system, and the card is declined even though the customer’s issuing bank has approved the payment.

This is called a soft decline, and you can usually resolve it by retrying the transaction.

On the other hand, there is not much you can do if a hard decline occurs.

Hard declines happen when the customer’s bank rejects the payment due to expired cards or security issues, such as a lost or stolen card or possible fraud. In that case, advise the customer to call their bank.

Source: Regpack

Don’t worry; you won’t be tasked with deciphering the nature of a decline. When a decline occurs, the merchant sees the relevant issuer decline code.

Sometimes you will also see an error message next to the code. Bear in mind that errors vary from gateway to gateway.

We’ll list two of our codes to illustrate the point.

For example, if you see a label Error code 10000 PAYMENT_GENERAL_FAILURE, this just means that a general payment failure has occurred, and it’s safe to retry the payment once or twice more.

However, the label Error code 14002: AUTHORIZATION_EXPIRED signals a hard decline. This code means that the issuing bank doesn’t approve the transaction because the authorization has expired. It’s not advisable to retry such transactions.

It’s best to get to know different credit card decline codes even before a decline occurs. To help you stay ready, we’ve compiled an exhaustive list of all of our payment error notices and the reasons behind them.

Don’t Limit Your Customer Pool!

Offer Multiple Payment Options Seamlessly

Communicate the Credit Card Decline Empathetically

Having a credit card declined can happen to anyone, but it still causes customers to feel embarrassed and uncomfortable. By communicating the decline message empathetically, you can assure them that you understand and value them as a customer.

If a declined payment happens in person, here’s how you can approach the customer:

- Stay inconspicuous

- Avoid arguing

- Maintain your professionalism

When a card is declined, you can tell the customer what happened without drawing the attention of others. Depending on the decline code, you can ask them to retry the transaction or ask if they have a different card.

Customers can react differently, but it’s important that you stay calm so you can resolve the situation quickly.

In case you’re accepting payments digitally, the same rules apply, but via different media.

There is a term used to describe the process of communicating with clients about payment failures: dunning.

The most effective way to reach customers is via dunning emails.

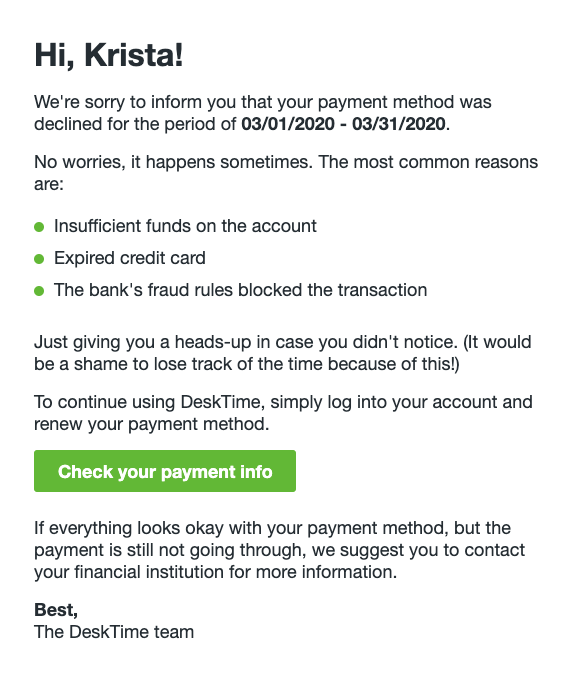

Here’s an example of a DeskTime dunning email:

Source: Baremetrics

As you can see, the finance team was understanding towards the declined payment. They even told the customer not to worry because it happens sometimes.

To prevent the customer from panicking, they listed the common reasons why cards are declined. Finally, they provided clear instructions on how the customer could solve the problem.

Notice how they didn’t make a big deal out of a declined payment. Still, DeskTime is a business that needs to get paid, so they made the repayment process easy and gave the customer directions.

Payment failures are bound to happen. Whether you’re dealing with online or offline interactions, the same principles apply.

If you approach declined credit card declines empathetically, you will reduce the awkwardness the customer feels and help them solve the issue.

Suggest Alternative Forms of Payment

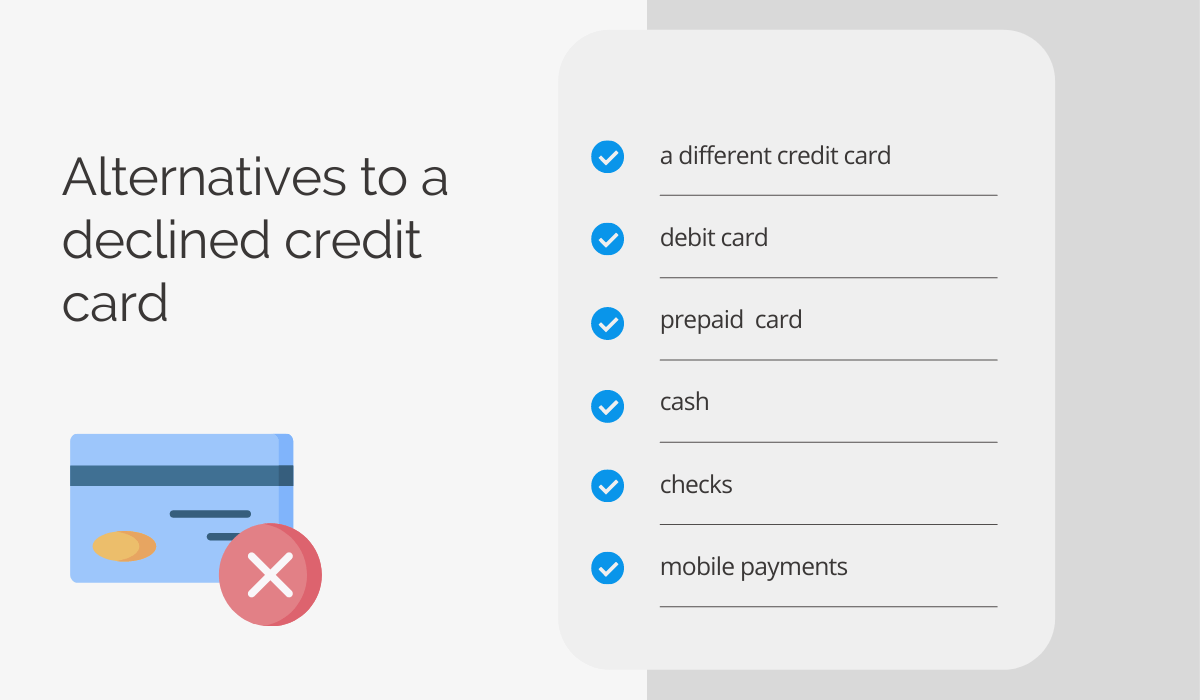

A declined credit card is not an unsolvable problem. To get paid faster, you can work with your customer on finding an alternative form of payment.

The first method of alleviating the issue is to try the same card again. Remember that you can only overcome soft declines by retrying.

When you recognize from the code that a hard decline has occurred, there is nothing a merchant can do; the customer has to contact the issuing bank.

If the payment isn’t accepted after a retry or two, it’s time to move on to other options. Not all businesses accept the same payment methods, so you should inform your customers which options you take.

Source: Regpack

According to an Experian 2020 review, an average American carries four credit cards. So, if one card is declined, it’s likely that your customer has another one in their wallet. You can also ask them if they have a debit card they can use.

Cash use may be on the decline, but it still accounts for more than a quarter of all transactions (26%), so it’s an option worth mentioning to your customers for in-store purchases.

Similarly, the frequency and volume of check payments are decreasing, but they are a valid payment method nevertheless.

As opposed to cash, check payments are linked with a customer’s ID. So, before accepting a check, see if the customer’s name and bank identification number are written correctly.

E-check is a digital alternative to a paper check, which is a useful option to have if you’re dealing with online payments.

Source: Regpack

Mobile payment usage correlates with age. Younger adults (18–34) are more likely to use a mobile payment service than their older counterparts–useful info to know if you have people of this age among your customers.

If the owner of a declined card owns a smartphone, you can ask them to pay with a service such as PayPal, Apple Pay, or Samsung Pay.

Decrease Non-Payment By 75%

With Flexible Payment Plans!

Mind the Costs of Declined Transactions

A declined transaction may not cost the customer anything, but it does cost the merchant. You have to pay the authorization fee for each declined card. The costs can accumulate, so you should track your expenditures closely.

Cards can be declined for a number of reasons. For instance, the EMV chip can get dirty, but when you retry the transaction after wiping the card, the payment goes through.

However, cards can sometimes be declined on the grounds of the issuing bank’s fraud protection protocols. When you retry a declined credit card, you’re actually resubmitting it for approval, so you are charged a fee for that service.

Different issuing banks have different decline rates. For example, U.S. Bank has a higher rate of declined credit card transactions compared to other banks. The highest rate of declined debit card transactions is visible at Chase Bank.

Yet, if you look at the following graph, you can see that the banks with the worst credit card decline rates perform better than those with the lowest debit card decline rates.

![]()

Source: Spreedly

This graph also tells you that even the most reputable banks, such as Bank of America and Wells Fargo, don’t have a zero rate of credit card declines, so you have to mind the cost of declined transactions regardless of the provider.

The cost of declined cards depends on your gateway and provider. Some don’t charge declined cards because no transaction has taken place.

Some, on the other hand, charge an authorization fee per transaction regardless of its success. This includes paying for card declines and voids.

While the fee may not be too high on an individual basis, ranging between $0.15 and $0.25, the cost of fees can rack up over time.

Let’s see how the declined fees can look like when they accumulate.

If you get a declined card two times a day and retry each three times at a price of $0.25 per retry, you’re paying the fee of $30 a month. That’s $360 a year.

This is why you have to be mindful of retrying the declined cards. If you notice an increase in the number of declined cards, you may want to contact your provider so you can act in advance and prevent unnecessary declines from occurring.

Review Your Payment Gateway Fraud Security Settings

A merchant themselves can’t control all aspects of the security of credit card payment processing; it’s the responsibility of the gateway.

But you as a merchant can choose a secure gateway and review its fraud security policies to keep your business a fraud-free zone.

There’s no business without customers, and today’s customers want their data secure. To cater to their customers, business owners place great emphasis on the safety and security of their customers’ data.

Still, don’t forget that protecting your data and finances is as important.

The single biggest action you can take to keep your business secure is to choose the right gateway provider.

Credit cards are often declined as a gateway’s precautionary measure. To curtail fraud, transaction processing systems often use overly-protective checks, which can cause false declines. These are usually solved by retrying the card.

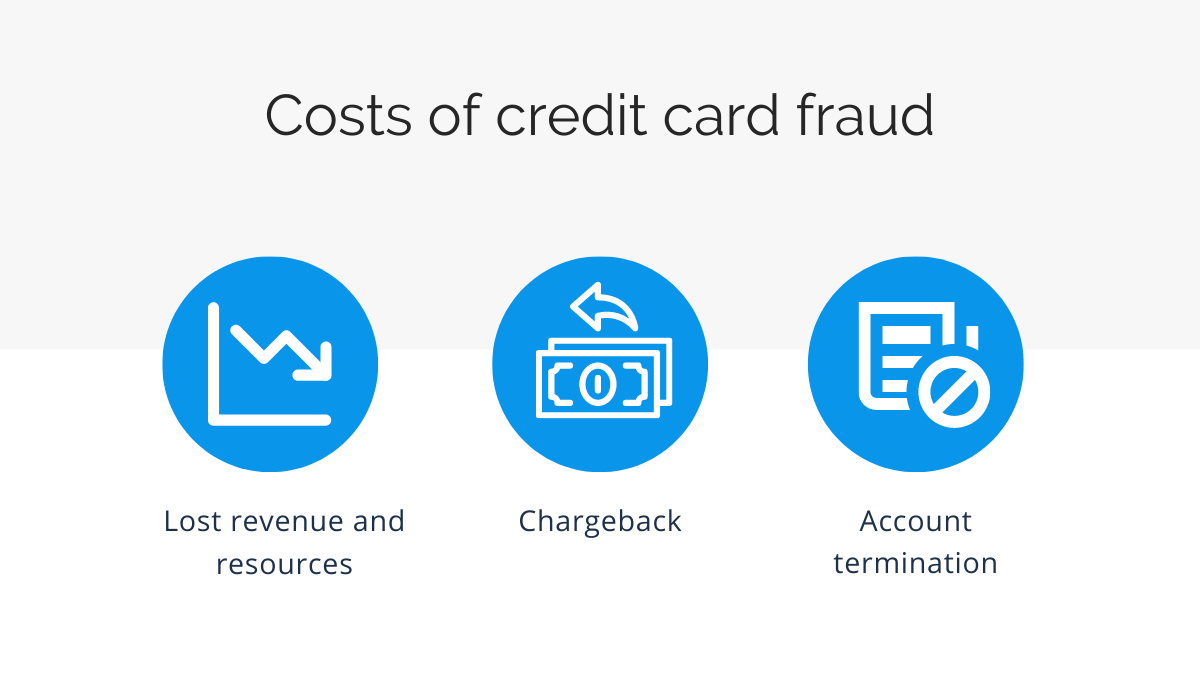

However, credit card fraud is a serious risk that causes multiple types of costs to merchants.

Source: Regpack

The most obvious cost is the lost revenue. If you ship out the product that wasn’t paid, you’ve lost resources as well.

If the transaction turns out to be fraudulent, you’ll have to deal with chargebacks: paying the customer’s bank back. Finally, too many chargebacks can lead to your merchant account being terminated.

To prevent such hindrances, you should work with a gateway provider that keeps fraud in check. Gateways use several methods to protect the data, and MyIMA Network has compiled a list of five security measures usually used. These are:

- Data encryption

- Secure Socket Layer (SSL)

- Secure Electronic Transaction (SET)

- Tokenization

- PCI DSS Compliance

You can use this list of criteria to choose the provider that can keep your and your customers’ data secure. When you select a provider, maximize the purchased service by enabling all the security features they provide.

Accept Payments Online, Right On Your Website!

Streamline your checkout process, offer payment plans, and more!

Plan for Credit Card Declines Ahead of Time

As unpleasant as they might be, credit card declines are inevitable. Led by the better safe than sorry principle, you should have a plan for such events and follow it to reduce your and your customers’ stress.

The plan for handling declined credit cards will vary depending on whether the transaction was done in person or online. Let’s see what you can do about in-store declines first.

Here’s a short overview of steps you can take when a card is declined. You can find a more detailed description below the picture.

Source: Regpack

So, when a card is declined, your first step should be to verify the data. That means checking the expiry date or checking the correctness of any data that may have been entered manually, such as the price entered on the POS terminal.

Looking at the credit card decline code will give you some insight into the seriousness of the decline, i.e., if it was a soft or a hard decline. Hard declines should be left to the customer’s bank to resolve. You can only retry the card in case of soft declines.

A good practice is to suggest alternative forms of payment before retrying the same card. Your customers could have cash or other cards with them. If not, you can retry the card–glitches in the gateways will usually sort themselves out.

Whichever actions you take, you should keep a record of the issue, its cause, and your solution. This may help you later if you need to fight a chargeback dispute.

For online purchases, you can add another step to the plan.

You can notify your customers ahead of time about upcoming payments. That way, they will have enough time to enter all their data without rush and avoid mistakes in typing their name, credit card number, or CVC code.

If online payments still fail, don’t worry. Sending dunning emails will help your customers notice the issue and get you your payment.

Conclusion

Since you can’t prevent all card declines altogether, you have to be prepared to handle them as they occur.

Remember that not all declines are equal, so they require different approaches depending on the situation. The credit card decline code can help you in establishing the route to resolving the issue.

Sometimes you can retry the card, but sometimes you’ll have to suggest a different payment method or ask the customer to contact their bank.

A good method of monitoring card declines and the costs they inflict is to keep track of any card decline that occurs. Using that information, you will be able to identify the most common causes of card declines and create a plan to tackle them.