There’s no such thing as the best merchant account provider for everyone. However, you can certainly find the best merchant account provider for your business specifically.

This post will help you find the most suitable option for you among the sea of providers. We’ll guide you through seven criteria and tell you why they matter.

By the end of this post, you’ll have enough information to narrow down your selection to the best options. You’re only an article away from accepting credit card payments, so let’s get started.

Jump to section:

They Should Suit Your Business Needs

They Should Provide Great Value for Money

You Should Understand All Contract Terms and Conditions

They Should Meet All Security Requirements

They Should Provide Great Customer Support

They Should Offer Sufficient Flexibility

They Should Allow Other Software Integrations

They Should Suit Your Business Needs

The search for the right merchant account provider should begin with analyzing your business.

Do you want to accept online credit card payments? What are your plans for the future? Define what you want from the provider and be clear about what your business needs.

There are many merchant account providers out there. But with six million employer firms in the US, they are easily outnumbered by the types of businesses they serve.

Each of these types of businesses will require different things from their merchant account provider. What works for an eCommerce business doesn’t have to work for a brick and mortar store and vice versa.

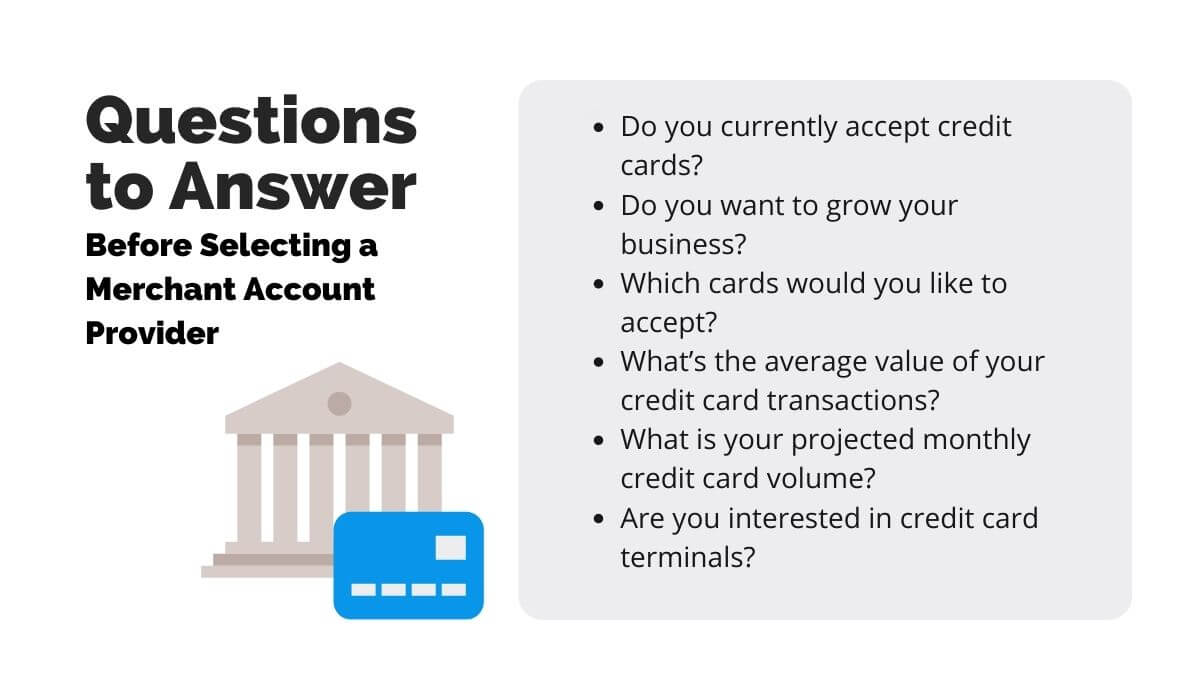

So, for instance, if you run a larger operation, you may want to invite your accountant for a meeting. Together, you can go through the questions from the following image to determine the requirements for your merchant account provider.

Source: Regpack

By answering the questions about your current payment practices, credit card transactions, and plans for the company’s future, you’ll build the foundation for defining the criteria for your merchant account provider.

For instance, if you’re planning to sell monthly meal plans, you can filter out all merchant account providers who don’t support recurring payments.

On the other hand, you don’t have to select a provider with the most features if you aren’t going to use most of them. Paying for more than you need will rack up the cost for no real reason. This brings us to our second criterion: price.

They Should Provide Great Value for Money

Paying for a merchant account is not a one-and-done process; there are several kinds of fees that go into it. You should examine your options prior to committing and settle for an option that’s affordable in the long run.

When you were starting up your small business, you probably had to deal with some unavoidable fixed expenses, such as office furniture.

However, a more significant share of the costs you pay are running costs, such as web hosting, rental space, or taxes. Keep in mind that merchant accounts also fall into the latter category.

Don’t forget that, other than a setup fee, you may have to pay for the following types of fees as well:

- Monthly fees

- Cancellation fees

- Per-transaction fees

- Online transaction fees

- Chargeback fees

If you decide on implementing a POS terminal as well, you might also have to pay for additional tools, hardware, and maintenance.

Merchant account fees can be charged as a fixed amount, a percentage of your sales, or a combination of both. Transaction fees are usually calculated as a percentage plus a fixed amount of money.

For instance, your provider may charge you 2% of each transaction plus 15 cents. So, if you sell an educational program for $100, you make $97,75. The amount of fewer than three dollars may seem insignificant, but don’t forget that fees accumulate.

Still, the fees that come with merchant accounts are worth it when you compare them with the profit you get from credit cards, one of the most popular payment instruments.

When choosing a provider, make sure to ask for a list of all possible fees.

And don’t forget that a more expensive provider isn’t necessarily a better one; price doesn’t always equal value.

Focus your research on the quality of services a provider offers, not the number of features you may not even need.

You Should Understand All Contract Terms and Conditions

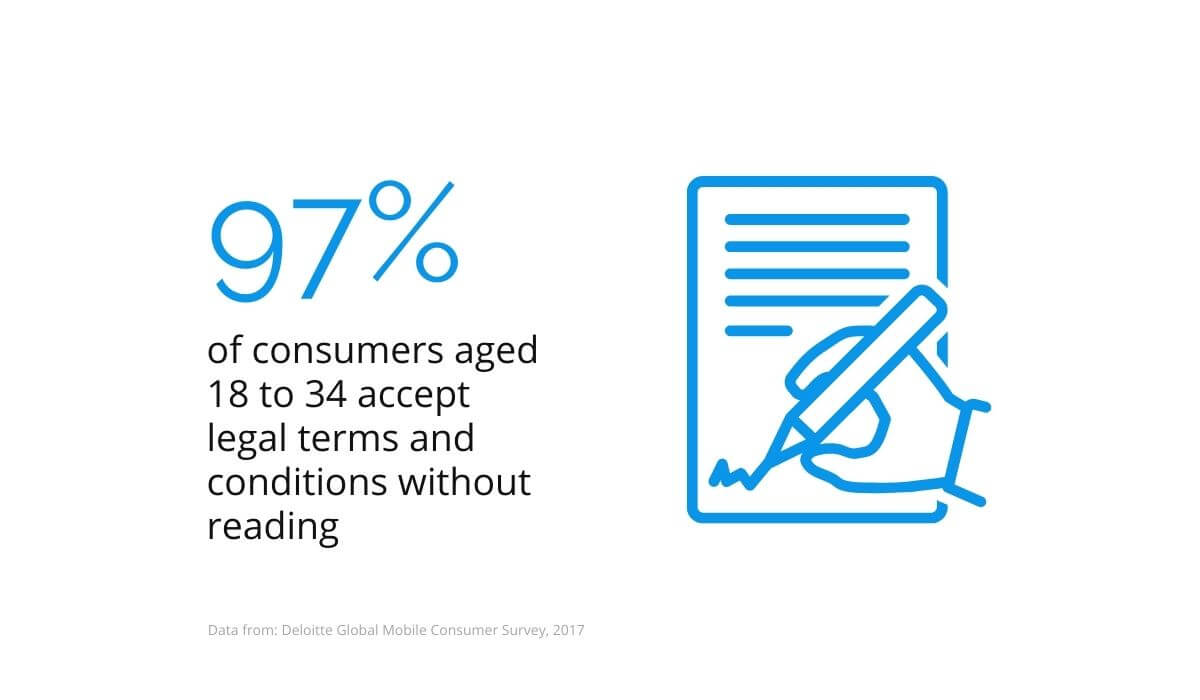

As a business owner, you’re probably familiar with the perils of fine print. Make sure to go through all contract terms and conditions, so you know you’re getting a good deal from your merchant account service provider.

Let’s kick this section off with a (not so) shocking fact: 91% of consumers willingly accept legal terms and conditions without reading. The percentage rises to 97% for ages 18 to 34.

Source: Regpack

Hopefully, you’re applying more caution when making business decisions than installing a game on your phone.

Once you narrow down your selection or choose the merchant account provider that best fits your needs, you should dedicate enough time to perusing the terms and conditions you’re about to sign.

It’s vital to familiarize yourself with terms and conditions before signing a merchant account contract.

As opposed to providers who offer month-to-month billing, some only work on a long-term contractual basis. In such cases, you should pay special attention to early termination fees (ETFs).

Here is some vocabulary you should look out for when reading your contract:

- Early termination fee

- Liquidated damages

- Equipment restocking or buyout fees

- Equipment lease early termination fee

You could even try to negotiate the early termination fee down so you can protect yourself from hefty costs down the line should you ever switch providers.

If you find legalese confusing, you’re not alone. More than half of consumers believe financial institutions purposefully use confusing jargon. If you have any doubts about the contract you’re signing, it could be helpful to seek legal advice before you put ink on it.

They Should Meet All Security Requirements

Credit card payments are not a one-sided process; they involve the data of you and your customers. Handling money is a delicate job, so remember to factor the security methods in your merchant account provider choice.

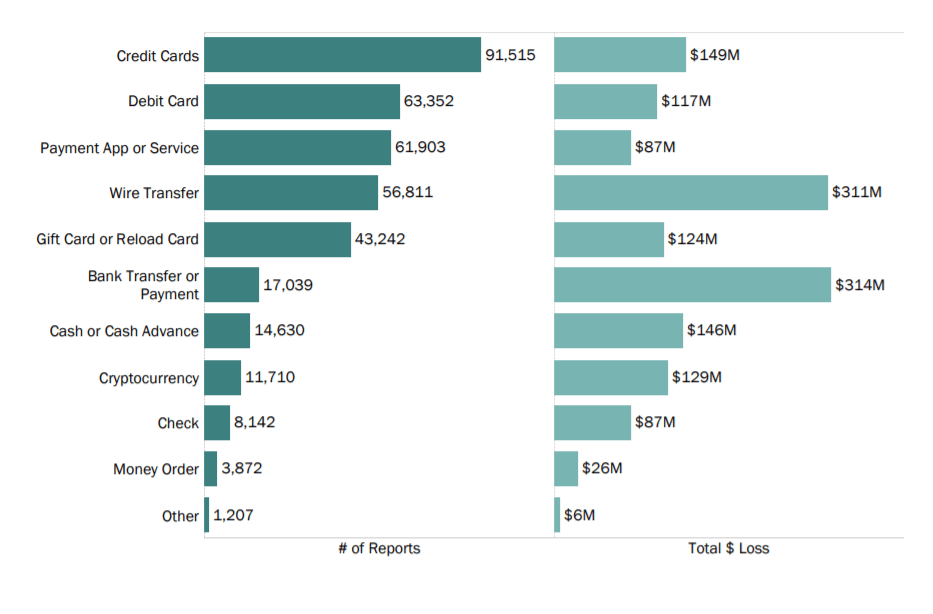

Credit cards may be one of the most popular payment methods, but they are also the most susceptible to fraud.

According to the Federal Trade Commission, a total loss of $149 million occurred in 2020 as a direct result of credit card fraud.

Source: Federal Trade Commission

Not all instances of credit card fraud are caused by hackers breaching advanced security systems. It’s usually the companies that make leaks and attacks easier by not configuring their software correctly.

More than half (66%) of organizations leave back doors open to attackers through misconfigured cloud services.

To fend off possible attacks, the third party you choose for credit card payment processing has to have the highest standards in safety and security.

Therefore, the first requirement you have to look for is the payment card industry (PCI) compliance standard.

The PCI standards were set to protect the customers’ payment card information through 12 requirements companies must meet.

Next, your provider has to encrypt the data they store. That way, even if third parties get access to the stored data, they won’t be able to read it.

While encrypting the stored data is a great defense against attackers, it’s even more helpful to reduce the amount of the data stored.

You and your merchant account provider should never store the track data held by the magnetic stripe, CVV, PIN, and PIN Block.

In addition to choosing the most secure merchant account provider, you can also do your part to protect the customers’ data. The active steps you can take are constantly updating your hardware and software and reporting any security suspicions as soon as they occur.

If you’re interested in an in-depth overview of best practices for securely handling customers’ credit card information, you can find our detailed post here.

They Should Provide Great Customer Support

Customer support is always important, but especially so in payment processing. If there are any issues with customers’ money, they want the solution immediately, which is why you need great, responsive customer support.

Let’s face it; if you ever have an issue in processing a payment, the customer will likely pinpoint your company as the source of the problem, regardless of the true cause.

However, a problem won’t tarnish their perception of you irrevocably if you resolve it quickly.

A study conducted by Harvard Business Review has found that the customers whose problems were quickly acknowledged and resolved by companies tend to remain loyal customers.

When it comes to processing card payments, to provide good customer support, you yourself should receive great customer support from your merchant account provider.

In fact, according to a Mercator Research report, better service is one of the top reasons why small businesses switch their card processing providers. Other reasons include lower costs and better reporting.

Source: Regpack

Ideally, your merchant account provider should offer live customer support, be it via live chat with agents or direct phone support.

At least 60% of customers would rather wait in a service queue to get help from a human than immediately receive help from a chatbot.

So, when you narrow down the list of potential merchant account providers, make sure that responsive customer support is one of the key factors that contribute to your decision.

Before signing a contract, ask the provider how you can get help should any problems arise. It’s safer to give preference to those with a trained in-house team rather than those who outsource customer support.

They Should Offer Sufficient Flexibility

The fact that you have a certain number of monthly customers now shouldn’t stop you from scaling up and down to suit your business. So, don’t forget to check if your selected merchant account provider supports the adjustment of services and plans.

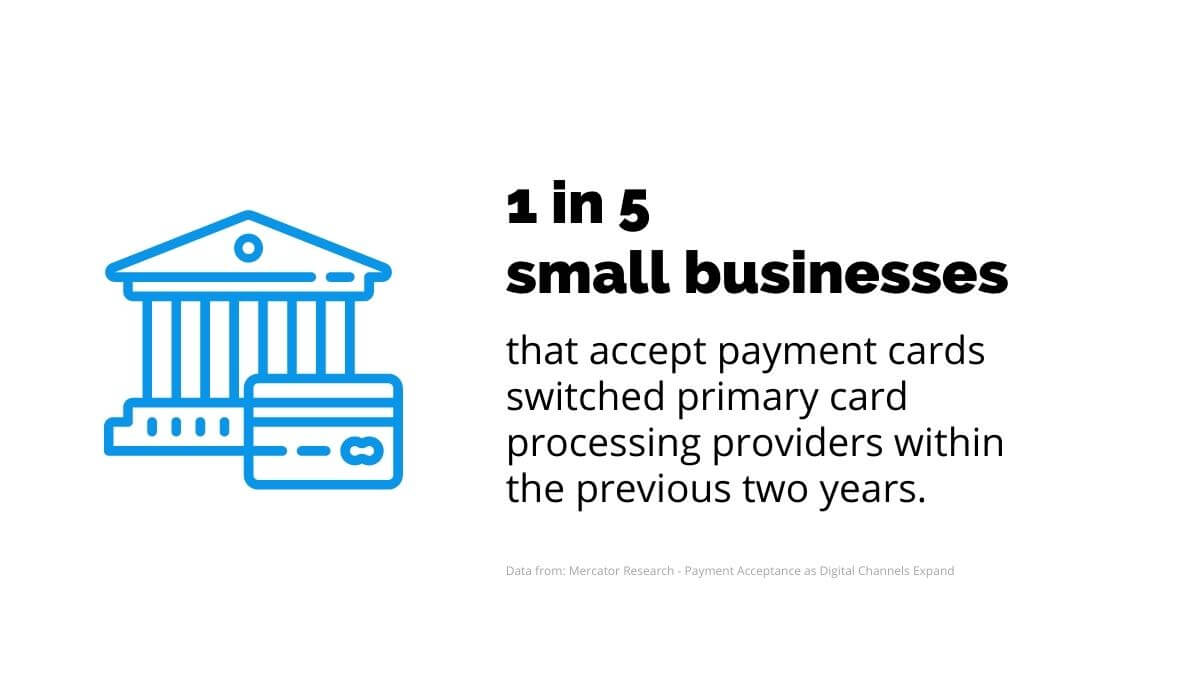

When you find a merchant account provider that fits your current needs, don’t lose sight of the word current, especially if you’re just starting your business.

Your card-processing needs may change over time. And it’s much easier to upgrade your plan than switch providers like one in five small businesses does.

Source: Regpack

Switching providers requires a lot of paperwork and maybe even some downtime, so it’s safer to ensure the possibility of altering the features you’re paying for later from the word go.

Whether you’re selling products or services at physical locations or running an online business, you never know how you will have to adapt your business.

For example, who could have seen how the Coronavirus pandemic would change the fitness industry?

After shutting down, many gyms have started selling digital fitness content, which affected their customer traffic. Not to mention the challenges of freezing or canceling memberships.

The point is, you have to look for a flexible merchant account provider.

Hopefully, your business will grow enough that you can introduce an online store, start accepting multiple currencies, or maybe start accepting recurring payments. Whatever the change, your provider should be able to implement it painlessly.

They Should Allow Other Software Integrations

Once you find a provider that meets your requirements and fits your budget, you should be able to integrate it into your store with ease.

Despite the trends in digitization, integration challenges persist. A 2021 Mulesoft connectivity study has found that 87% of surveyed organizations find that difficulties with integration hinder their digital transformation.

So, a merchant account provider won’t necessarily boost your business if you struggle with setup and maintenance.

This is why it’s wise to directly ask the provider how long the integration takes or if they provide training on using the system.

Since merchant account providers create their products with regular business owners in mind, the process of integrating payments into your online store should be possible without advanced coding knowledge.

Source: Regpack

Merchants who sell goods or services at physical locations should also take into consideration the implementation process for a POS system and other pieces of hardware.

After all, one of the reasons companies switch their POS provider is that the POS system is too hard to use.

Remember to also check for integration options for external software, such as with apps you may be using for accounting.

Let’s take QuickBooks, a prominent accounting solution, as an example. The solution is so sought after that many merchant account providers highlight the feature of integrating with Quickbooks.

Of course, you’ll check for other software integrations according to your needs, but it’s important to know that you should look for this option when choosing the best merchant account provider.

Conclusion

Merchant account providers are not one size fits all. To ensure you’re getting your money’s worth, choose one depending on your business model and business needs.

The relationship between the price and the value you get should also impact your decision, as should the provider’s customer support capabilities.

Make sure to select a secure solution that is easy to integrate. If you’re considering a long-term partnership with your provider, don’t forget to check how you can alter your plans if needed.

Before committing to a provider, the final step should be carefully examining the terms and conditions; you don’t want any surprises in later stages.