In the highly digital world we inhabit today, e-commerce businesses live or die by their ability to carry out secure, smooth, and speedy online transactions. Integral to these transactions are entities are known as “merchant acquirers” and “payment processors”. They may sound like interchangeable terms, but they play distinctly different roles in the payment ecosystem.

An understanding of these roles is essential for anyone involved in e-commerce. In this article, we’ll break down these roles, explain how they work, and ensure you thoroughly understand the difference between a merchant acquirer and a payment processor. Before we do that, let’s get to grips with what these terms mean.

A merchant acquirer, which is also often referred to as an “acquirer” or “acquiring bank”, is a financial institution that maintains the merchant’s account. It receives all transactions from the merchant to be processed.

On the other hand, a “payment processor” is a company often a third party appointed by a merchant, that handles payment transactions for merchant acquiring banks. Its job is basically to manage the transaction process, by transmitting transaction details from the merchant to their acquiring bank, and then to the cardholder’s bank (the issuing bank), and finally back to the merchant’s bank.

Now, you might wonder – why are we at Regpack talking about this? Well, we’re an online registration and payment management platform trusted by thousands of organizations worldwide. Our work is closely related to both payment processors and merchant acquirers, so we’re in a pretty good position to share knowledge about these crucial terms. So, sit back, and let us guide you through the nitty-gritty of “merchant acquirer vs payment processor”.

In the following sections, we will discuss more in-depth the roles of merchant acquirers and payment processors, the differences between them, and ultimately, how our platform, Regpack, can provide an effective solution to streamline these functions. Let’s dive in!

Understanding the Role of Merchant Acquirers

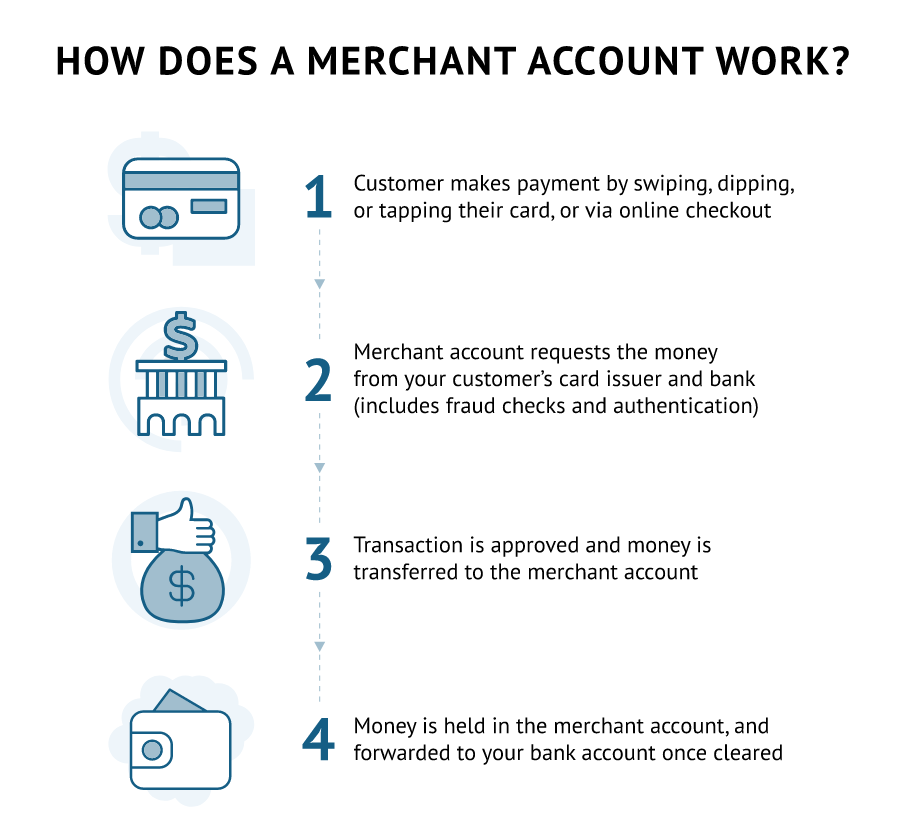

To fully grasp the concept of a merchant acquirer, it’s essential to dig deeper into the roles they play in the payment process. As we’ve mentioned briefly, a merchant acquirer or an acquiring bank is a licensed member of a card network, such as Visa or MasterCard. They have a direct relationship with your business – the merchant. When your business enters into an agreement with them, they provide you with a merchant account that enables you to accept card transactions, both credit and debit card payments.

Now, let’s delve into how merchant acquirers actually facilitate these transactions. When a customer decides to make a purchase from your store using a credit or debit card, the acquiring bank plays a vital role in ensuring the transaction’s success. Once the customer’s card information is entered, the acquiring bank verifies the details and checks whether the customer has sufficient funds in their account. If all details are correct and there are sufficient funds, the acquiring bank approves the transaction.

This transaction process isn’t limited to just checking the funds. Merchants and customers alike need assurance that their data is secure. Merchant acquirers provide a safe and secure ecosystem for processing these card payments. They are responsible for transmitting customer data securely to ensure that the transaction is processed without any data breach.

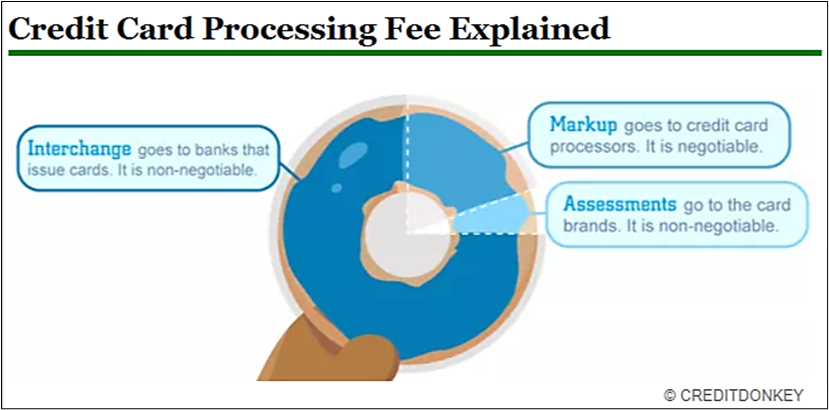

Now, you might be wondering about fees. Well, for the services they provide, merchant acquirers charge a fee. This is often referred to as the interchange fee, a necessary cost for merchants who desire to offer card facilities to their customers.

Furthermore, merchant acquirers offer payment processing services, enabling businesses to accept online and digital payments. These services help businesses operate efficiently and competitively in a world where more purchases are being made online every day.

To sum things up, the role of merchant acquirers in the payment ecosystem is of utmost importance. They facilitate businesses to operate in the online market, ensuring smooth, safe, and secure transactions. In the next section, we’ll be exploring the role of payment processors to shed more light on how these two entities function in synergy.

Unveiling the Workings of Payment Processors

Converse to merchant acquirers, payment processors wear a slightly different hat in the transaction process. To begin with, payment processors, as the name suggests, are responsible for processing payments between the merchant’s bank and the customer’s bank, which is also referred to as the issuing bank.

In the payment ecosystem, a payment processor plays the role of a mediator. When a customer uses a debit or a credit card to make a purchase, the payment processor ferries the relevant transaction details between various entities. Their role becomes even more vital in the electronic payments’ dynamic landscape, where transaction speed is crucial, and delays can result in sub-par customer experiences.

This might make you think that the payment processor bears a great deal of responsibility, and that’s true. It essentially provides the infrastructure used by an online business to access the payment gateway, which connects the merchant, issuing bank, and the acquiring bank. Any hiccups in this infrastructure can lead to payment failures or delays that can often lead to lost sales.

Now, let’s talk about third-party processors and issuer processors. While third-party processors essentially service the merchant, issuer processors connect the cardholder’s bank. An issuer processor ensures that the debit card payment or credit card payment is appropriately debited, communicates the transaction status back to the payment gateway, and ultimately follows the chain back to the merchant’s account.

You may also come across the term “payment facilitator model” in some contexts when talking about payment processors. A payment facilitator is often a service provider authorized by a merchant acquirer to enable transactions for sub-merchants. They essentially take on the role of the merchant acquirer for a variety of smaller merchants, which may not have the necessary resources to establish a direct relationship with large financial institutions.

In essence, the payment processor is the middleman in the card payment transaction, ensuring smooth communication and transaction execution. It streamlines the payment process, making it easy for merchants to receive payments from customers promptly and safely.

Merchant Acquirer Vs Payment Processor: What’s the Difference?

While both merchant acquirers and payment processors play their part in ensuring the end-to-end completion of a payment transaction, their roles are different. We’ve studied their individual roles and responsibilities; now, let’s highlight their critical differences and their interaction within the card network.

Starting with the transaction process, a payment processor essentially acts as a bridge between the merchant, the acquiring bank, and the customer’s issuing bank, as we’ve discussed. A merchant acquirer, on the other hand, maintains the merchant’s account and is a direct link to the card network.

The payment facilitator is technically a subset of the payment processor. It operates under the umbrella of a merchant acquirer, creating sub-merchant accounts for smaller businesses – often in a shared environment. This simplifies the process and access for small-scale merchants, who may not have the wherewithal to establish a direct relationship with a large financial institution.

Next, let’s talk about the banks. The acquiring bank is partnered with, typically maintained by the merchant acquirer. The issuing bank, penning the customer’s side of the transaction, is the institution that communicates with the payment processor. Understanding this distinction is crucial: while both entities work with banks in the payment ecosystem, they work with different banks serving different purposes within the transaction process.

The interchange fee, a critical cost in card transactions, is charged by the merchant acquirer for maintaining the merchant account and facilitating the payment processing. Payment processors, on the other hand, may charge a fee for accessing their payment infrastructure and covering costs associated with the transaction process.

In essence, both merchant acquirers and payment processors have distinct functions in the card network. Still, they interact synergistically, playing their individual parts to ensure a seamless experience for businesses and customers alike.

Now, you understand how both of these entities run their course in the payment journey. In our next section, we’ll talk about the role that Regpack plays in this complex ecosystem, and how our solutions help simplify these processes and boost your business’s efficiency.

The Importance of Regpack’s Payment Processing & Merchant Acquiring Systems

Now that we’ve elucidated the roles of merchant acquirers and payment processors let’s discuss how Regpack’s system streamlines these processes.

At Regpack, we understand the needs and challenges faced by businesses in managing their payment transactions. As a trusted payment service provider, we designed our system to address these bottlenecks effectively, aligning with the payment facilitator model.

Our system ensures a smooth transaction process by seamlessly managing the connection between your business, the customer’s issuing bank, your acquiring bank, and the card network. Our platform is built to simplify the complexities involved in debit card transactions, credit card payments, and online payments. Be it a customer making a purchase via American Express, Mastercard, or Visa, our system handles all payment methods efficiently.

Enhancing security in transactions is at the top of our priority list. We adhere to strict security protocols safeguarding your payment information and your customers, ensuring each transaction is safe and secure. We also understand that not all businesses may have a direct relationship with large financial institutions, which is why we facilitate the role of a payment facilitator to provide smaller businesses the means to accept card payments.

Choosing Regpack for your payment management results in not merely owning a system that processes payments. Instead, you are investing in a platform that values the importance of each transaction, offering superior security, and helping your business maintain a competitive edge in the digital economy.

References:

“What is a Payment Processor” NerdWallet, https://www.nerdwallet.com/article/small-business/what-is-a-payment-processor. Accessed November 13, 2023.

“Merchant Acquiring” Payment Institutions, https://paymentinstitutions.eu/wp-content/uploads/2017/08/Merchant_acquiring.pdf. Accessed November 13, 2023.