The surge in online transactions, spurred by the pandemic, remote work, and a growing number of online payment methods, has put businesses under pressure to ensure secure payment processing for their customers within a frictionless shopping experience.

If you’re running an online store, you need to know how to best protect your customers and your business from fraud, cyberattacks and other risks looming on the web.

These six tips will help you understand various aspects of secure payment processing and improve your practices.

- Follow the PCI Security Standards

- Refrain From Collecting Too Much User Information

- Use Payment Tokenization

- Encrypt the Data

- Use Strong Customer Authentication (SCA)

- Perform Regular Security Audits and System Enhancements

- Conclusion

Follow the PCI Security Standards

The process of strengthening the security of your online store starts with your business complying with the Payment Card Industry (PCI) security standards.

This will enable you to gain trust from your customers, prevent data breaches, and help you avoid fines and credit card processor restrictions.

The standards were developed in 2014 out of a need to keep data safe.

They represent a set of guidelines that ensure that all businesses that handle credit card information do so in a secure environment.

The Payment Card Industry Data Security Standard (PCI DSS) was developed jointly by major credit card brands (Visa, MasterCard, American Express, JCB, and Discover) and is overseen by the Payment Card Industry Security Standards Council (PCI SSC).

Source: pcisecuritystandards

They defined four PCI compliance levels according to the number of annual card transactions processed by a business.

For instance, if you process over 6 million card transactions a year, you’ll be categorized as a level 1 merchant. This means you’ll be obliged to meet the strictest PCI DSS requirements.

On the other hand, if your business handles less than 20,000 transactions per year, you’ll be classified as a level 4 merchant, and achieving PCI compliance will be that much easier.

Keep in mind that, although they established PCI DSS together, each card brand implements its own levels.

For example, Visa categorizes businesses with up to one million transactions as level 4 merchants, while MasterCard has kept the original PCI SSC classification, meaning that such businesses are level 3 merchants.

For more information on what businesses must do to achieve PCI DSS compliance, you can use the PCI Compliance Guide.

Source: pcicomplianceguide

In their FAQ section, you’ll find detailed info on, for example, what small-to-medium-sized businesses should do to become PCI compliant. The process involves filling out a self-assessment questionnaire (SAQ) and submitting it, along with other evidence, to your merchant bank, i.e., your acquirer.

Payment processors (mediators between you and your bank) also have a key role in helping you achieve, maintain, and manage PCI compliance.

Still, it always pays to understand and proactively handle your obligations.

In conclusion, PCI compliance is mandatory for all businesses that want to accept card payments.

It helps you avoid data breaches and fraud that can seriously hurt your bottom line and brand reputation, driving away both existing and new customers.

Refrain From Collecting Too Much User Information

Keeping the data you collect from your customers to a minimum will reduce the harmful consequences of data breaches and leaks while also providing a smoother customer experience.

That’s why you should refrain from collecting too much user information.

Let’s first consider some numbers.

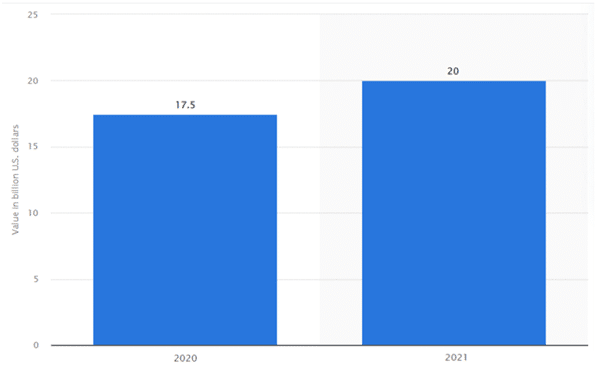

As the chart below shows, e-commerce businesses lost a whopping $20 billion in 2021 to online payment fraud, compared to “only” $17.5 billion in 2020.

Source: Statista

This is a 14% year-to-year jump fueled by the recent explosion of e-commerce and a steep rise in related frauds that naturally followed.

If you minimize the amount of information you require from your customers, the less likely you are to be adversely affected by such breaches.

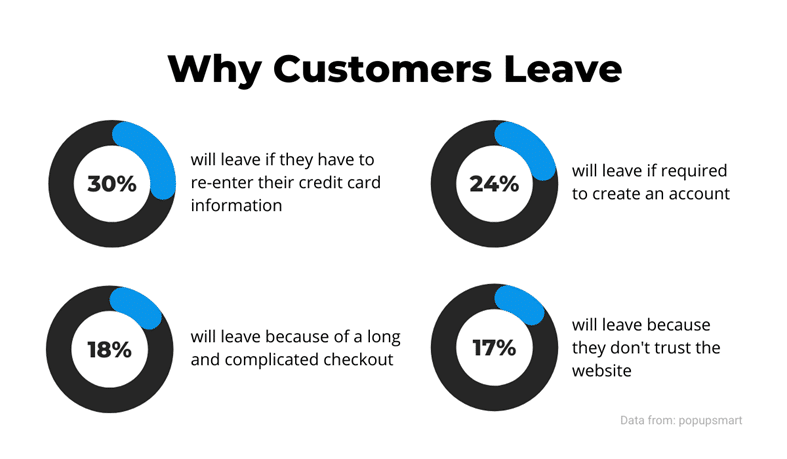

As for providing a good user experience, the numbers below show different reasons why customers abandon their shopping carts, all of which may be related to asking for too much information.

Source: Regpack

Therefore, there are many good reasons why you should streamline your checkout process and keep the information collected by your website to a minimum.

For example, when it comes to card payments, you need only the card number, cardholder name, expiry date, and the security code (CVV2, CDC, CID).

Unfortunately, some websites still ask their users to select a card type, although it can be automatically determined from the first digits they enter, thus increasing friction.

In addition to collecting only the necessary information, there are several ways to make the checkout process more user friendly.

For instance, consider offering a guest checkout option where the customer’s information is used only to process their order and then deleted.

It is also a good idea to integrate the sign-up process with popular services like Facebook, Gmail, or Apple.

Naturally, many service providers offer the resources required to protect your customers and your business from fraud and cybercrime, such as Stax.

Source: staxpayments

Hence, refraining from collecting too much user information is a precaution that can help you avoid chargebacks and penalties related to fraud and security breaches, while also keeping your customers happy and ready to shop with you again.

Use Payment Tokenization

Although both encryption and tokenization are common solutions businesses use to protect sensitive data like credit card numbers or personally identifiable information (PII), tokens offer enhanced security features.

So, why not go with the latest technology to make both mobile and desktop payments as safe as possible?

Payment tokenization is a technology that converts customers’ sensitive data into random, indecipherable unique identifiers (tokens).

In other words, they don’t use the key as encryption does. Instead, tokens hide information behind randomly generated values.

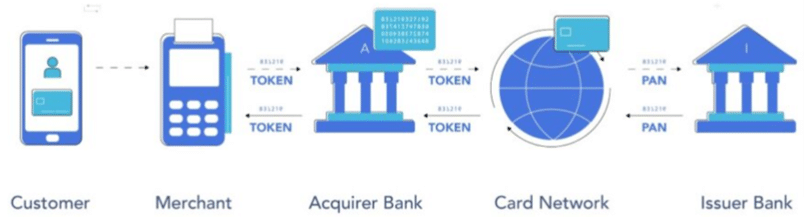

Before tokenization, when a customer bought something with their credit card, the primary account number (PAN) they provided was encrypted and sent to the payment processor, after which it was stored in the merchant’s internal system for future reference.

When transactions are tokenized, the customer’s card number goes through a tokenization system first. Here’s how this process works.

Source: mymoid

Since each token is randomly generated and assigned to each piece of sensitive information, there’s no key code that hackers can crack to read all the information protected by that specific encryption key.

Tokenization removes sensitive data from the company’s internal systems, so there is nothing (useful) to steal even if those systems are breached.

And it also acts as a safeguard against fraud.

According to Visa’s survey, clients who use tokenization can expect fraud attempts to drop by at least 25%.

Furthermore, tokenization can be used to expand your payment options, thus increasing the reach your online store has.

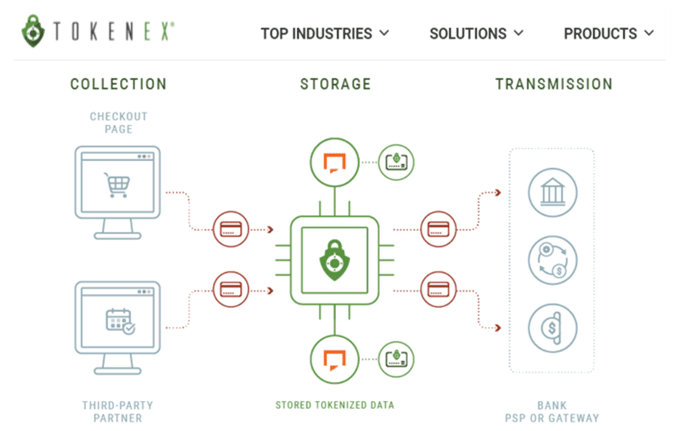

For example, Snaptravel, a booking engine, used the TokenEx platform to tokenize credit card information from third parties, thus reaching another 10% of their target market.

Here’s how that solution works.

Source: TokenEx

Tokenization also facilitates compliance with PCI DSS. And, as PCI certification can be costly for businesses, many are using already PCI compliant payment providers like the one above.

Thus, if you want to make your customer’s data even safer, consider using payment tokenization.

Encrypt the Data

Data encryption is a cornerstone of digital data confidentiality.

Without it, our communications on the web and other networks would be exposed to multiple risks.

Thus, encryption is the golden standard of secure payment processing that protects your business from losing money and customers due to data breaches and fraud.

Recent Identity Theft Resource Center’s research shows that over 90% of data breaches result from cyberattacks.

So, ensuring that your customers’ online payments are secure is critical. And this starts with the internet security protocols your website is using.

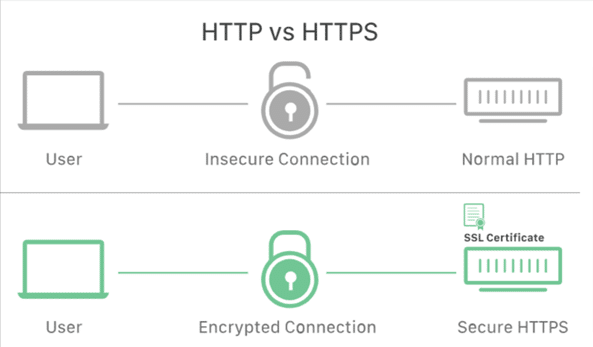

The one protocol with three names that’s considered a must-have when secure online communication is concerned is Hypertext transfer protocol secure (HTTPS).

It’s the encrypted and thus secure version of HTTP.

Here’s the difference courtesy of Cloudflare, another provider of end-to-end payment security solutions.

Source: Cloudflare

The HTTPS address, lock icon, and green bar mean the website has a Secure Sockets Layer (SSL) certificate.

And, although it’s still called SSL, this usually refers to a Transport Layer Security (TLS) certificate. Hence, the three names wrapped into one—HTTPS.

The most important thing to remember here is that HTTPS is mandatory if you plan to accept online card payments. It is a PCI compliance requirement.

Secondly, it’s quickly becoming synonymous with secure web browsing.

Source: Google

Thirdly, both users and Google prefer it. According to Google’s Transparency Report, Chrome users spent 93.2% of their browsing time on HTTPS pages.

As for Google’s preference, HTTPS has been a confirmed Google ranking factor since 2014. And visitors of all sites not using HTTPS have been warned about that fact since 2018.

So, Google has been actively promoting its use. In their words:

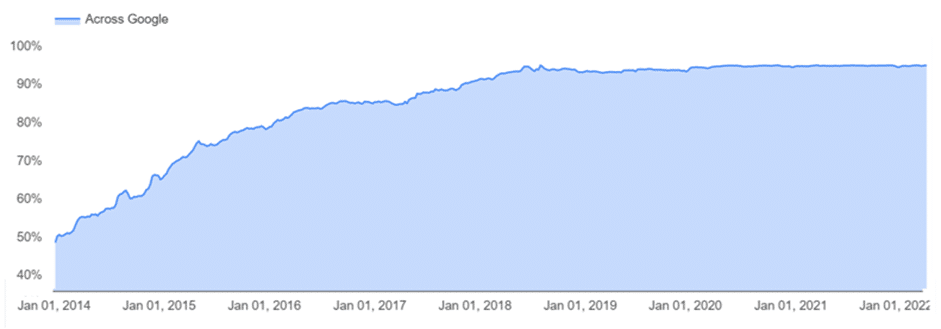

“We are investing and working to make sure that our sites and services provide modern HTTPS by default. Our goal is to achieve 100% encryption across our products and services.”

And here’s how that’s going:

Source: Google

You can see that the current percentage is about 90%.

However, this number is only going up as new web platforms are, as a rule, made available only to sites working on HTTPS.

You can learn more about encryption on Google’s HTTPS FAQs.

Thus, data encryption in general and HTTPS, in particular, are not just recommended but crucial for protecting the privacy and security of online communications.

As such, they represent an essential element of ensuring secure payment processing for your customers.

Use Strong Customer Authentication (SCA)

If your online store is based in Europe, you have already heard about Strong Customer Authentication (SCA).

And if your US-based store has European customers, you should be aware of the changes they’re going through and how that affects your business.

Ultimately, you might want to use SCA to protect your business from online transaction fraud.

SCA is a new requirement stemming from the second Payment Services Directive (PSD2).

Aimed at preventing transaction fraud, it requires European banks to ensure additional user authentication before approving payments.

SCA came into force in 2019, and its enforcement began in 2020.

It’s still ongoing because many EU countries have opted for a staggered approach.

For example, full SCA enforcement started in the UK on 14 March 2022. You can see the latest planned enforcement dates here.

Source: Stripe

Although SCA implementation is lagging in some EU countries, payment processors and e-commerce merchants around the world are increasingly following suit to avoid potential rejected transactions from European banks.

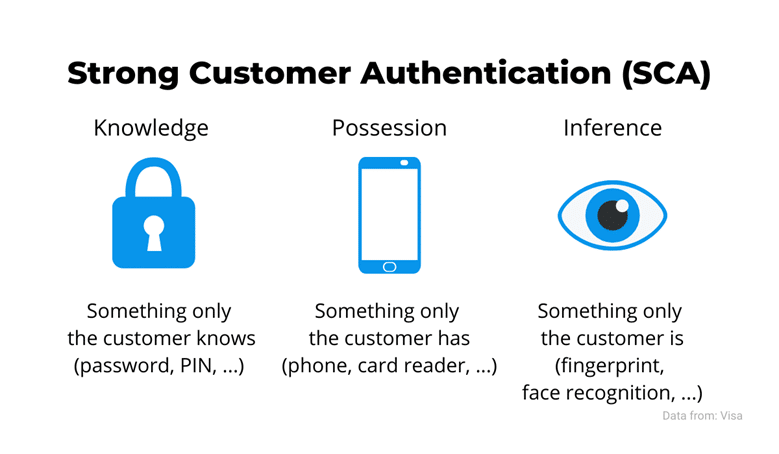

What does this regulation do?

It prescribes that payment service providers must authenticate customers by using at least two of these three factors:

Source: Regpack

As many other countries are introducing their own SCA versions, it’s clear that it will become the next globally accepted standard for secure online payments.

And although the US e-commerce stakeholders are still unaffected, it’s just a matter of time when SCA will become the norm here as well.

Naturally, some solutions take care of this for you, such as Stripe.

Source: Stripe

This suite of payments products provides customizable SCA-ready solutions that will monitor different SCA enforcement deadlines and apply authentication and exemptions accordingly, thus minimizing user experience friction and avoiding a higher number of declines from European banks.

All in all, it’s evident that SCA adoption is coming.

So, why not get ahead and look for the best SCA solutions for your business?

It will cut down on credit card fraud and chargebacks, thus increasing the payment processing security and reducing costs.

Perform Regular Security Audits and System Enhancements

Performing regular security audits and updating your systems is the one element that integrates your entire payment processing strategy.

Audits and system enhancements will ensure that your business stays ahead of the latest threats, thus preventing cyberattacks and associated costs and ensuring smooth and secure payment processing.

As said, the skyrocketing e-commerce growth also created more opportunities for various forms of cybercrime.

The 2022 SonicWall Cyber Threat Report showed that ransomware attacks worldwide increased 105% in 2021 vs.2020.

On a country level, the US is a little better (+98%), while the UK is “under attack” (+227%).

Their report also refers to other types of cybercrime on the rise, such as IoT malware, cryptojacking, and encrypted threats.

SonicWall offers protection against all of them. For instance, here’s what their website says about preventing encrypted attacks.

Source: SonicWall

As you can see, scanning of encryption protocols and system updates are crucial for effective protection against cyber-risks, which brings us to the importance of conducting regular IT security audits.

Although their frequency depends on many factors like company size, industry, etc., most companies do them once or twice a year.

These audits are carried out by information security auditors who test the system’s performance against a list of specific security criteria.

An audit can be complemented with a vulnerability assessment and penetration testing (VASP), two further tests.

The first one looks for system vulnerabilities, and the second attempts to exploit them.

Penetration or pen testing is done by pen testers, or ethical hackers who try to hack your system and see which vulnerabilities detected in the vulnerability assessment (scan) can be used for malicious attacks.

Naturally, there are different tools that will help you with this, like nessus.

Source: tenable

And serious businesses take their security seriously.

For example, our payment processing software, Regpack, is PCI-2 compliant and will help you create custom payment forms and accept payments online securely.

Our security protocols are rigorous—our code, databases, and servers are automatically scanned every hour, while our servers are manually checked every day.

Pen testing is performed every week.

As for official PCI audits, we have been passing them all on the first scan since 2010.

Source: Regpack

In summary, regular security audits and system enhancements are critical for ensuring secure online payments.

They help you identify security weaknesses, establish robust security policies, and discover new vulnerabilities, thus preventing costs related to cybercrimes and protecting the reputation of your business.

Conclusion

So, it’s clear that ensuring secure payment processing for your customers requires a comprehensive approach to the security of your IT systems.

This will require the services of third parties, such as your payment processor and merchant bank, and the use of specialized software and expertise.

We hope that the above six tips helped you better understand the basics of cyber-security in today’s world and showed you how you could safeguard your business from data breaches and fraud, thus protecting your customers, as well as your reputation and profits.