Small businesses often struggle with financial planning. It’s a complex matter, and there are so many financial metrics to consider and so few employees to deal with them.

However, financial planning (or lack thereof) is the most critical element in determining whether your business is successful or not.

It gives you a vision and guidelines to help you stay focused on the essentials.

In this article, we’ll share some valuable financial planning tips that will allow your small business to turn that vision into reality.

- Set Attainable Financial Goals

- Consider the Top Risks Your Small Business Could Face

- Create Cash Flow Projections

- Maintain Accurate Financial Records

- Plan Your Taxes Properly

- Plan Finances Using Business Funds Only

- Create a Business Succession Plan

- Conclusion

Set Attainable Financial Goals

Some small business owners achieve success simply by getting lucky. They have no clear financial plan in place and figure things out as they go.

Although it works for some businesses, this kind of passive approach only leads to problems in the long run because no one knows what they’re working towards.

Instead of leaving things to chance, a much better way to run a business is by implementing a financial strategy with clearly defined goals.

According to Square:

Source: Square

Financial goals provide direction to the organization and workers, who will feel more driven to do something once they know what the end goal is.

This sense of purpose translates into increased efficiency, as your employees work better as a better team to get the company where you want it to be.

Set goals help you track progress and constantly improve. Reviewing your performance monthly or quarterly is a great way to ensure that you stay on track.

Each time you check how far you’ve gotten, you will see what the situation is like in reality instead of what you imagined.

You can then redistribute resources as needed, for instance, from a segment ahead of schedule into one that’s not going according to plan.

Naturally, financial goals should be attainable. Goals are attainable if they are realistic and make sense for your company specifically and not just in general or for another business.

For example, if you want people to register for a trip to a place that can accommodate 50, you can’t set your goal at getting 60 registrations because it’s not attainable – there is no room.

A vague and generalized objective, like making money, also doesn’t work because there’s no benchmark for what “making money” actually means, so 100,000 dollars can be a lot for small companies and barely anything for large corporations.

A much better approach is to set specific goals that work for your company, and make it time-bound, such as “making 27,000 dollars in profits by July 2022”.

That way, you have a specific amount and date when you should achieve your goal, so you know precisely what to focus on to meet that deadline.

Consider the Top Risks Your Small Business Could Face

Taking risks is an integral part of owning a small business, and you wouldn’t have your company if you weren’t willing to take them.

Still, having faced some risks doesn’t mean that you’re prepared for all of them.

This seems to be the case for many small business owners—Embroker’s Big Risks for Small Businesses report shows a gap between what small and medium enterprise (SME) owners perceive as risk and what they’re focusing their efforts on.

Their top 3 concerns were related to reputation, product failure, and labor issues.

Source: Regpack

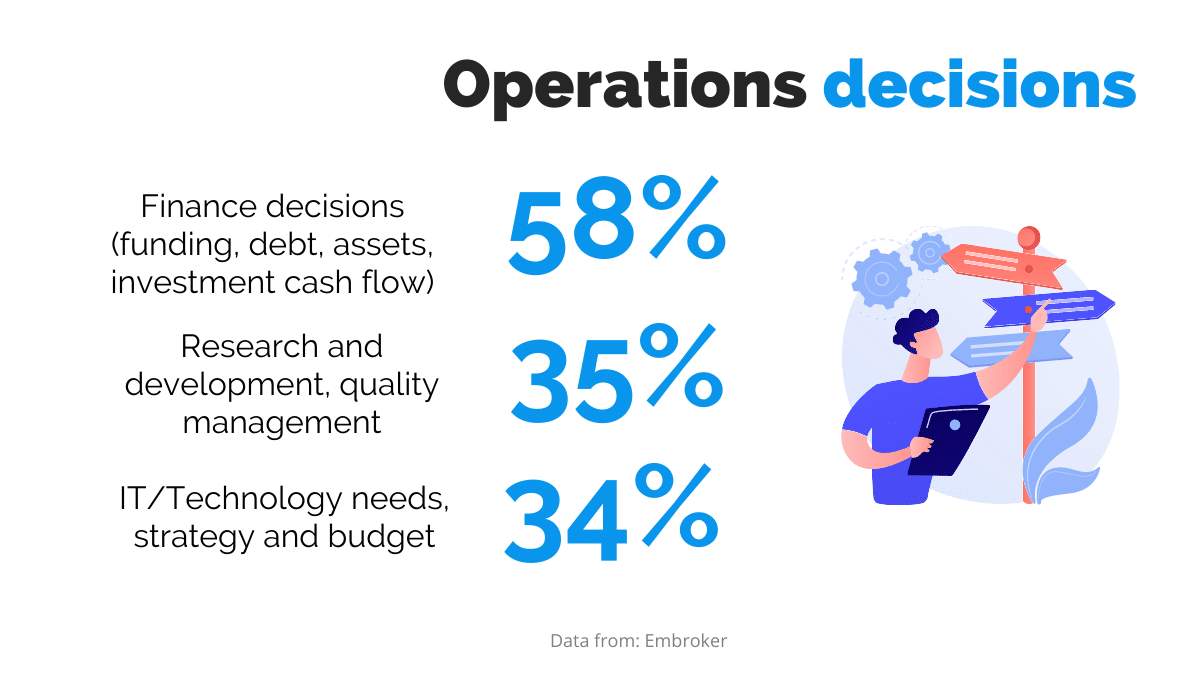

However, they still focused their efforts on finance, research and development, and technology.

Source: Regpack

As you can see, there is no correlation between the perceived level of risk and actions taken to mitigate them.

Another thing you can notice is that financial decisions top the operations decisions by a wide margin, which goes to show that risks ultimately affect your finances.

So, what other types of risk are there?

The U.S. Small Business Administration (SBA) roughly divides them into two categories:

- Internal risks

- Human risks (illness and death, theft and fraud, low employee morale)

- Equipment and IT risks (faulty equipment, cybercrime)

- Other (injuries and damages, cash flow issues, damage to reputation)

- External risks

- Competition and market risks (market changes, employee turnover, rent increase)

- Business environment risks (legislation changes, weather and natural disasters, changes in the community)

Naturally, nobody expects you to prepare for every possible outcome, but what you can do is create a risk management strategy for the top risks that your business could face.

Identifying them might take some time, so a good idea is for you and your team to look for anything that can hurt your profit or that is a growth obstacle.

It will vary depending on your industry and the type of business you run, so think about it carefully and revisit the list often. You can use ISO guidelines for risk management to help you.

Even better, consult professionals.

Companies in the risk management industry that have experience with small or medium enterprises are more likely to identify risks you might not see coming, e.g., those stemming from growth opportunities or investments.

When you know what threats you can realistically expect, you can find ways to eliminate or mitigate them and plan your finances accordingly.

Let’s say you find out that other companies in your line of business have been experiencing data breaches.

Even though you may not have planned for it initially, you can now reorganize your financial plan and allocate funds for more secure and encrypted solutions or security awareness training for your employees.

That way, you will be prepared and minimize additional costs that would inevitably arise from a cyber attack.

Create Cash Flow Projections

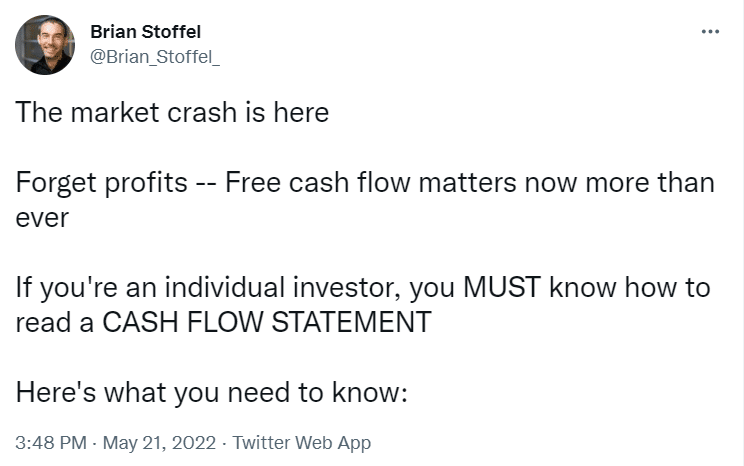

Financial journalist Brian Stoffel recently tweeted that free cash flow matters now more than ever.

Source: Twitter

However, as most small business owners know all too well, maintaining a positive cash flow is hard.

Many clients, particularly large corporations, offer extended payment terms to increase their own cash flow, even though this hurts the small and medium enterprises they owe money.

In addition, many business owners aren’t aware of the importance of cash flow, with 82% of SMEs in the USA citing poor understanding or management of cash flow as the main reason for failure.

Without understanding how money goes in and out of your business, it’s difficult to make informed decisions and know when to save and when to spend.

This is where cash flow projections come in handy. A cash flow projection is a breakdown of a company’s income and expenses, or accounts receivable and accounts payable.

It’s essential in short-term financial planning because it shows how much money your business is expected to have at the end of each month.

The term is sometimes used interchangeably with a cash flow forecast but Fluidly states that the key difference is that a forecast is the most likely scenario, while projections factor in multiple hypothetical options and then create a best- or worst-case scenario.

It seems complicated, but a practical step-by-step guide can be found here.

You can also use many tools to help you, from software solutions to a Microsoft Office template for small businesses or an American Express template.

Cash flow projections help with early risk detection.

For instance, if you’ve noticed that a client you invoiced in January hasn’t paid you, and you wanted to buy new equipment in February, you could postpone the purchase to March, when the cash flow is expected to be better.

An overview of your cash flow will help you identify potential risks and eliminate them before they become significant issues.

Move the pieces of your cash flow schedule as needed to make decisions based on real data to cover your expenses and have a healthy cash flow every month.

Maintain Accurate Financial Records

You can’t plan ahead if you don’t know your current financial situation, so keeping accurate financial records is essential for the future of your business.

Financial records reflect your company’s financial stability.

They are valuable to you, for knowing how your business is doing at all times, and also to people you decide to cooperate with, be it partners you want to work with or loan officers who approve your loan.

Staying on top of your finances can be straightforward if you’re a sole proprietor, but if you’re a limited company and have more complex financial needs, it would probably be best to get some help.

You can get it by hiring a bookkeeper or an accountant.

Even though their roles are similar, they have different functions: a bookkeeper organizes finance and keeps records, while an accountant can provide analyses and offer tax advice.

In addition to people, another thing that can help you is accounting software. Even if you use software just for registrations and payments collection, like Regpack, you can get accurate insights into a part of your finances.

Source: Regpack

With Regpack, you can manage registration and payment from a single source, making income management more effortless and straightforward.

Bottom line, having software do your accounting reduces the chances of errors that are bound to happen when you do things manually. Your financial records will be impeccable, which will show your potential partners or investors that you take your business seriously.

If you’re considering expansion, all the information you need is within reach, allowing you to generate reports, make forecasts and do financial analyses before you finally make a decision.

Plan Your Taxes Properly

Whether you like it or not, every transaction you make has tax implications.

With that in mind, it’s always better to plan your taxes instead of trying to prepare everything when the filing deadline comes.

Taxes are a central part of your yearly financial planning, so it makes no sense to do them once a year. What you should do instead is create a comprehensive tax strategy.

As a small business, you want to exercise financial prudence to save as much as possible, and with effective tax planning, you can.

The first step to strategic tax planning is consulting a professional.

Even though the IRS website is also helpful and has useful tools (such as a calendar with reminders), a dedicated tax expert will help you determine what state and federal tax laws you need to comply with and advise how to do it efficiently.

They will also point you in the right direction as there are many tax deductions that you might not even know about.

For example, did you know that you might qualify for a deduction if you work from home? That’s just one of the many valuable pieces of advice a skilled accountant can give you.

Even better, the fee of hiring them is fully deductible, so it’s a win-win situation.

The next step is to see what expenses can be deducted and then keep detailed and itemized records of everything.

Software subscriptions, office supplies, utilities, and advertising – are just a few of the many things you can take advantage of.

You can consult QuickBooks’ complete 2022 list of small-business tax deductions to see what else can be deducted.

Once you’ve figured out your available tax deductions, you need to keep records of all your relevant purchase receipts, contracts, and other documents because you will add them as proof to your tax form.

Staying on top of your taxes and using all means available to reduce your tax liability ahead of time will save you money, ultimately allowing you to make better financial plans for the future of your business.

Plan Finances Using Business Funds Only

As a small business owner or even a sole proprietor, it’s understandable that your personal finances are closely tied to your business funds.

You probably used your own funds to start it, and you pay yourself a salary, so the business feels like an integral part of your life, if not your personality.

Maybe you even count on your personal finances as an additional source of revenue when the going gets tough for your business.

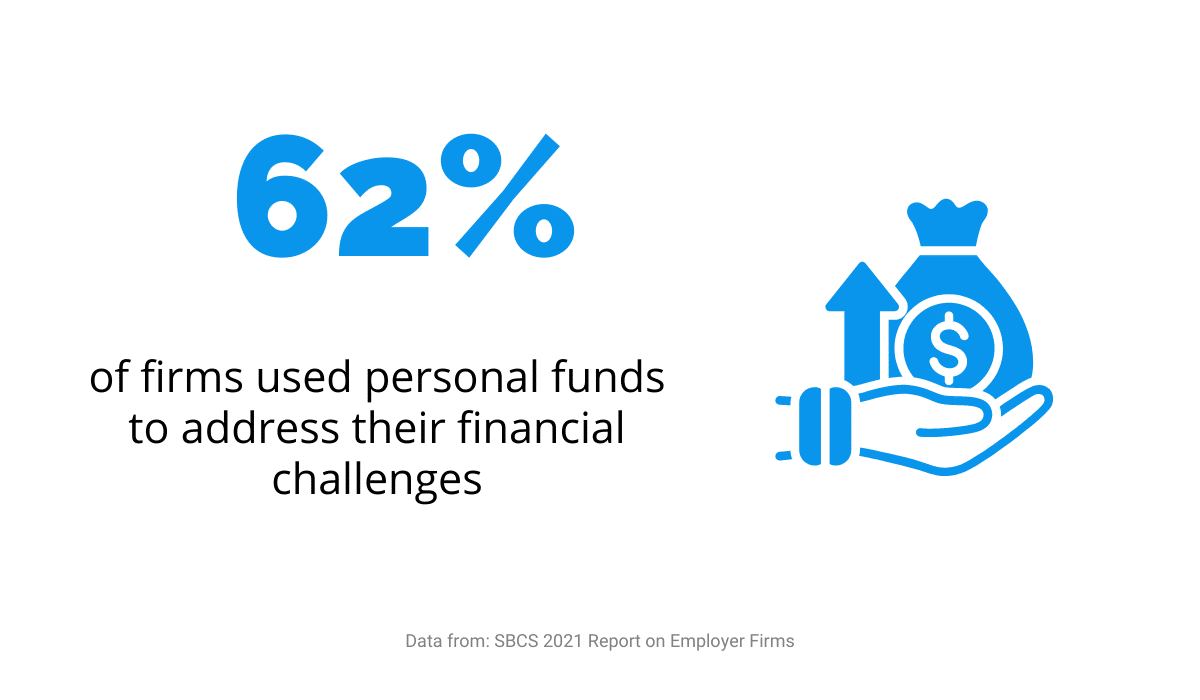

The Small Business Credit Survey (SBCS) 2021 Report on Employer Firms found that in 2020, 62% of small businesses used their personal funds to tackle their financial challenges.

Source: Regpack

If more than half of the companies did it, it’s ok to do it, right?

Not quite.

First of all, your personal financial situation can quickly change.

Consider the following: you count on your personal savings to be able to afford a new printer for your business in the next quarter.

You make plans around it, or even arrange jobs that require you to use it.

Suddenly, there’s a medical emergency, and you need to dip into your personal savings to cover the hospital bill.

Injuries, divorce, relocation, unfortunately, even death—those are just some things that can dramatically change your personal financial situation.

Even though these things have a significant impact on your life, if you don’t include your own money in planning the finances for your business, they don’t have to affect your company.

A good business owner always plans realistically, instead of hoping for the best-case scenario.

This means that you shouldn’t calculate potential funding either.

The fact that you applied for a loan does not guarantee that you’ll get it, so adding it to your available funds might lead to an overly optimistic budget estimate.

Instead of relying on your personal funds and hypothetical loans, LearnHub suggests doing these concrete things instead:

- Identify any capital required

- Create a balance sheet

- Produce a cash flow statement

- Project your future earnings

The good news is that if you’ve listened to our advice and maintained accurate financial records, half of the work is already done.

With a little bit of additional drafting, a master plan for your finances should be finished in no time.

Create a Business Succession Plan

Nobody likes to think about what their company would look like without them, but for small business owners, it’s unavoidable.

You’ve set up your own company, and it’s been running successfully, but you will have to step down eventually.

Unforeseen events can also prevent you from doing your job, and someone has to continue your legacy.

You should therefore be involved in the decision-making process about your company’s future and its current and future employees.

The best way to do it is to create a succession plan.

A thorough succession strategy is essential for your financial planning because having a plan for future scenarios helps you mitigate any risks connected with them.

Instead of unexpected events and the uncertainty resulting from them, there will be a guide to enable your business to continue running like a well-oiled machine.

Without it, your company runs the risk of losing significant amounts of money.

How?

Without a proper plan in place, there might not be a suitable replacement for you or another top executive within your company once it’s time to find one.

You will have to post a job ad, interview candidates, train them, and maybe even pay them more than you would for promoting someone within your own company.

On the other hand, a succession plan will have a ready solution for this, so all your future employees will have to worry about is the paperwork.

How can you create a good succession plan?

According to Society Insurance, the first thing is to identify a list of critical positions and a list of positions with a high turnover rate.

The former is essential because having highly skilled employees in these positions ensures that your company operates efficiently.

The latter is also not negligible because you can use it to identify why employees leave and address it or make plans for hiring new people.

The next thing is to identify employees’ skills to see who would be a good fit for each position and what steps are needed to get them there, including training and education.

This is where your business succession plan directly impacts your financial planning.

All training- or hiring-related costs need to be factored in to make informed decisions about when to hire and how much money you can afford to spend on a particular training program.

All you need to do next is assemble a team of high-quality employees and start working on your succession plan.

Once you make it, don’t forget to let your employees know that you have plans for them to move up in your company.

Seeing that there are opportunities for them to grow within the company will keep them motivated, thus increasing the likelihood of your succession plan being a success.

Conclusion

Being proactive instead of reactive is the key to the long-term success of your business.

The best way to do this is by setting attainable goals and making realistic plans for predictable events, such as taxation or audits, and unforeseen situations, such as risks or stepping down from your leadership position.

Instead of leaving things to chance, you will take your company’s future into your own hands, which is the quality of a true leader.