Integrating payment options for your B2B company is one of the last steps you will be taking before opening for business.

You've developed an excellent product or service, surrounded yourself with capable staff, and chosen your business model. The last thing you want is to lose clients at the final stage because your payment options are scarce or your payment process is complicated and unsafe.

But, have no fear; we're here to help.

This article will provide you with essential information on every payment method available to you, complete with advantages and drawbacks.

It will also draw your attention to billing software and automated systems that will make processing payments a breeze.

Cash

When discussing payment methods in the context of B2B services, cash is often left out of the equation.

To cover our bases, we are including cash in this list because it's still a valid B2B method of payment. It has discernable benefits and, if you want your business to stay agile, it can sometimes be the best payment option available.

In some cases, cash really is king.

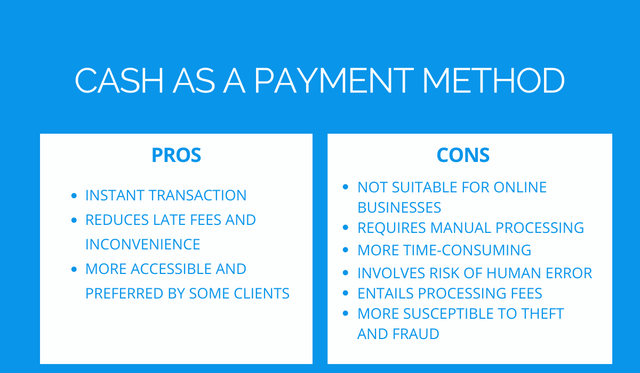

The most obvious advantage of taking cash is that it's instant. Once money changes hands, the transaction is completed. Therefore, taking cash can help you avoid late fees and inconvenience.

You may also find that cash is more accessible than other payment methods and preferred by some clients. Therefore, not including cash as a payment option may cause you to lose a client here or there.

Of course, this doesn't apply to the SaaS business model where everything happens virtually, but it is worth mentioning.

On the other hand, cash payments have serious drawbacks.

Cash is not an automated method of payment and needs human involvement and manual processing.

As a result, it may take businesses more time to make cash payments visible in the account, and there is an increased chance of human error.

Consequently, cash payments end up being a very costly method. The cost of handling cash may be as high as 4.7 - 15% of the amount owed when you factor in bank charges and surcharges for defective notes and courier costs.

Finally, cash increases access to your funds. However, having large sums of money available makes your business more susceptible to theft and fraud.

The takeaway is that cash can definitely complement your business practices, which is why you shouldn't gloss over it that easily. However, it may be best to include the method without emphasizing it to your clients.

See your numbers

Get a personalized, no-commitment savings report.

Have a question?

Ask Regpack AI anything.

Checks

Checks are another traditional payment method. However, checks show no sign of going out of style, unlike cash, which is showing a rapid decline in usage.

In fact, checks accounted for 80% of B2B payments in 2020, making them a payment option to include.

With so many transactions and such a long history, checks have evolved to be one of the most easily verifiable payment methods available to any business.

That's an important point because an essential advantage of this method is that checks are universally accepted.

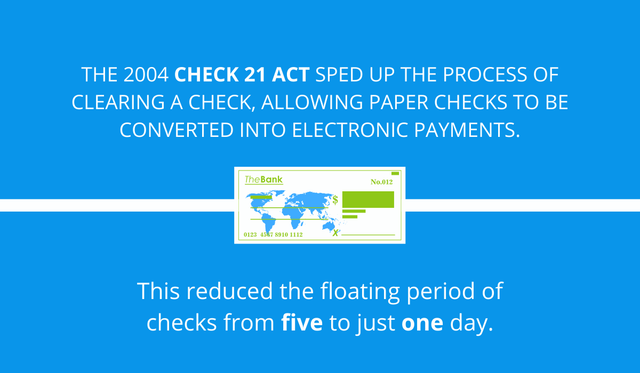

Since the 2004 Check 21 Act, checks have also become a much faster method of payment. Before Check 21, paper checks needed to be physically carried or mailed to the bank for the payment to be cleared.

The Act sped up this process by allowing paper checks to be converted into electronic payments, cutting the floating period of checks from five to just one day.

Checks are reliable and fast, no question. Nevertheless, this payment method comes with disadvantages of its own.

If you're accepting checks but are not in the vicinity of your clients, your clients cannot hand in their checks in person. Instead, they will send their checks in the mail.

This means that the payment process will be delayed for the time it takes for the check to reach you. Not to mention the risk of the check getting lost in the mail.

International transactions can also be problematic. Some US banks may object to taking a foreign check, and the delays caused by international mail are substantial.

Additionally, modern cloud-based businesses such as eCommerce or SaaS cannot take checks as payment. However, with electronic checks, that option becomes available.

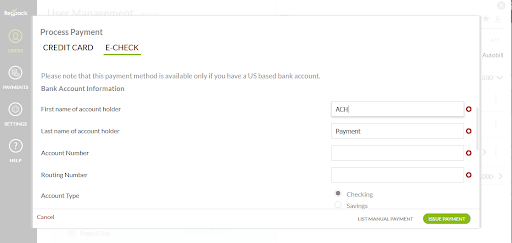

E-Checks

This is where our discussion on B2B payment methods veers into more modern practices.

Electronic checks are payments made online and have the same function as classic paper checks.

Payers can use eChecks for any transactions that a paper check would cover, and eChecks are governed by the same laws and regulations that apply to paper checks.

WIth digitized checks, money is withdrawn from the payer's checking account, sent over the ACH network (which we will talk about later), and deposited into the receiver's checking account. They are only offered in the US.

Since e-checks are online payments, they are alternatives to credit card payments and are also accepted by some online-first businesses. For example, our billing software allows users to accept eChecks as a way of payment.

Paper checks remain a crucial part of the US economy, and almost nothing can beat their reliability.

However, since they are a traditional payment method, SaaS or eCommerce companies need alternative payment methods such as eChecks for their online-first business model.

Credit Cards

Credit cards are one of the most popular payment methods for B2C businesses. Their foray into B2B is, however, more recent.

Right now, B2B payments account for about 1% of all credit card transactions. But card use is rapidly expanding. From $523 billion in 2018, B2B payments might exceed $763 billion in 2022.

Accepting credit cards can make your life easier. Businesses can sync credit card payments with accounting, CRM, and ERP systems for a fully automated payment process.

That means that credit cards are a fast payment method, made even faster because credit card payments are quickly cleared.

Also, credit cards are relatively safe. The probability of fraud and theft is low. If it does occur, credit companies have systems in place to buffer the effects. For example, by offering refunds.

With all of this in mind, it's interesting to note that many businesses still discourage their B2B clients from using credit cards to pay for services.

More often than not, this is because credit cards can be pretty expensive for the payer. Credit card fees can cost anywhere from 2.7 to 4.4% of the value of the transaction, meaning you're losing revenue.

Why is this more of a problem for B2B than B2C transactions?

Because B2B transactions are usually much larger than B2C.

Finally, accepting credit cards as payment carries a relatively high risk of failing to charge the client due to card expiration.

There's much to consider with credit cards. As a payment method, they are convenient and offer an excellent user experience for both sides of the transaction. However, they are also expensive and sometimes risky.

Debit Cards

The differences between credit and debit cards as payment methods are subtle but important. An optimal payment policy should include both methods.

In contrast to credit cards, debit cards don't incur debt on the part of the payer. They draw funds directly from the payer's checking or savings account to cover the cost.

Debit cards carry less risk for providers because the card user has to have sufficient funds to complete the transaction.

For this reason, debit card fees are significantly lower and are capped at 0.05% of the value of the transaction plus 22 cents. That also means less revenue lost for your company. These rates can differ depending on the card features, though.

Because the risk is low, debit cards get approved faster. In fact, debit cards are much like cash in that respect. They make for instant transactions.

Debit cards (as well as credit cards) are the preferred payment method of eCommerce and SaaS. If your company falls into this realm, you should account for both types of cards.

The drawbacks mostly have to do with cash flow on the part of the customer. If the payer doesn't have sufficient funds in their account, the transaction won't go through. This is one of the reasons why debit cards work best in combination with credit cards.

Accounting can be a bit more complex with debit cards. The companies processing debit card payments will send statements that need to be reconciled with the client's bank statements to confirm payments have come through.

This can cause errors and complications, so make sure that the person in charge of reconciliation has the necessary training and experience.

To reduce the possibility of error and ensure transactions run smoothly, many companies turn to automated systems, such as Regpack billing software.

Obviously, debit cards are a preferred payment option by companies everywhere. There's no fuss involved, and the costs are minimal.

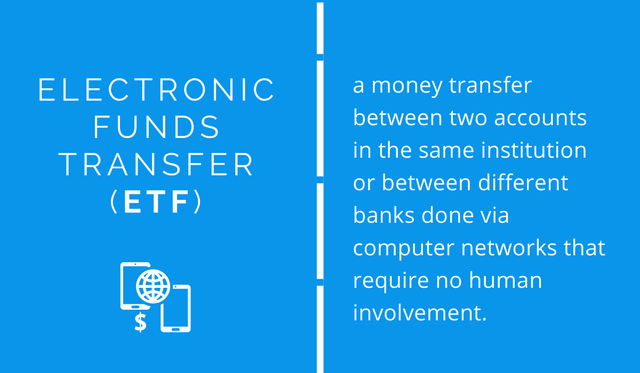

Electronic Funds Transfers (EFT)

Debit card payments and e-checks are actually part of a larger system of direct electronic money transfer from one account to another, along with direct deposits, ATMs, ACH, and wire transfers.

These payment types come together under the umbrella term Electronic Funds Transfer (ETF), an essential term for B2B accounting.

In a nutshell, EFTs are money transfers between two accounts in the same institution or between different banks done via computer networks. There is no human involvement.

The very definition may already give you an idea of what the benefits are.

EFTs are very practical, almost instantaneous, and available nearly everywhere. They don't require cards of any kind, just a bank account.

They also carry a low risk of error and failure. EFTs are covered by the Electronic Fund Transfer Act (EFTA) which protects consumers and suppliers involved in electronic transactions.

Sounds ideal, yes, but EFTs have their disadvantages, just like all other kinds of payments.

Once again, available funds can be an issue. This is why it's essential to complement your payment options with credit cards.

Additionally, EFT banking is impossible to do anonymously. If your customers expect a degree of anonymity, EFTs need to be complemented with more anonymous methods, such as cash.

Finally, low risk doesn't mean no risk. EFTs can still "bounce" and fail, although at much lower rates than checks and cards.

Two kinds of EFTs deserve special attention as B2B payment methods: wire transfers and ACH transfers.

As these are popular forms of payment used by B2B companies everywhere, we will cover them in more detail in the following two sections.

Wire Transfers

Wire transfers and ACH payments are quite similar, but they use different systems you should take note of.

It's not that one method is superior to the other. Rather, wire transfers and ACH payments are applied to different types of payments to produce the best results.

Wire transfers use the SWIFT network to deliver funds from one account to another.

Without going into too much technical detail, let's just say that this network is an information system that connects banks worldwide. It's a way to send and receive secure information, including information about money transfers.

Wire transfers will also be of use to you for international payments because banks everywhere use the SWIFT network. Additionally, this is the best method for larger transactions because wire transfers are not subject to cross-border payment limitations.

The disadvantages of wire transfers lie in their speed, cost, and security.

It takes a few days (usually 1-4) for funds transferred this way to be visible in the payee's account. Wire transfers are also very costly.

Banks can charge the sender up to $30 for individual transfers. This means you either have to include the bank fee in your price or accept the loss of revenue.

Security may also be a concern. Wire transfers are processed very quickly, and once they're completed, they're irreversible. This makes businesses using wire transfers a target for scammers.

To sum up, wire transfers are optimal for international transactions, but they are less safe, so make sure your clients are careful when making payments.

Automated Clearing House (ACH) Payments

ACH transfers are similar to wire transfers in many ways, but they have some clear advantages.

It comes as no surprise that ACH payments may be overtaking wire transfers to become the dominant method for B2B payments.

This payment method utilizes an older network called the Automated Clearing House, which operates within the US exclusively.

This is the method of choice for domestic transactions because it's significantly cheaper than wire transfers. Bank fees for this type of transfer will rarely exceed $1 for business transactions. Even better, the more ACH transactions you complete, the cheaper they become.

ACH payments are also reversible in cases when errors or fraud occurs. That makes them safer than wire transfers. A good payment processing software will allow you to process ACH payments as well like Regpack does.

Keep in mind that the risk of fraud and theft is never zero. Although safer, ACH payments need to be monitored carefully by your accounts payable management staff.

Since the Automated Clearing House is a US institution, international payments cannot be completed with this system.

Well, technically, they can. If a foreign client insists on transferring money, they need to bypass their country's clearing institution (such as the Single Euro Payment Area for the EU) and use the ACH. This process would be complicated, so it's better to encourage wire transfers for international payments.

Finally, clearinghouses and banks clear payments in batches at a set time of day, making this process relatively slow.

ACH payments can take up to three days. In other words, you may not be able to access your money for a certain time. This may strangle your cash flow.

All in all, ACH payments are a sure bet for your day-to-day business needs within the US. They're safe and cheap, but they may take a little longer to clear. Be sure to plan accordingly.

Payment Gateways

Payment gateways are vital for business models that rely heavily on online transactions and interactions, such as SaaS and eCommerce businesses.

Payment gateways are essentially software that can be fully integrated into your website to automatically handle payments from customers without the need for staff involvement. They can process direct payments, debit cards, and credit cards, depending on the system.

They are the automatic cashier at the end of the customer journey. They take the payer through a couple of simple steps to pay for the goods in their electronic basket.

Popular examples of payment gateways include the ubiquitous PayPal and Stripe.

Payment gateways are efficient and convenient to use, especially for smaller companies whose transactions fluctuate from month to month.

Keep in mind that payment gateways are not as established as check transactions and ACH payments and there are still some drawbacks.

For one, payment gateways are rarely universal. That means that almost no gateway accepts every card. This may significantly affect international users working with payment gateways specific to their own countries.

Another issue is security. Payment gateway users have reported problems with data breaches and malware. This is a rare occurrence, however, and payment gateways are mostly secure.

With the rise of the SaaS business model and more businesses going online, payment gateways are often the first step but are surpassed as the companies see a need for a more integrated solution.

The Importance of Billing Software

With large volumes of clients and many transactions carried out, it's obvious that a lot can go wrong if payments are handled manually. That's where billing software can help.

Billing software automates the payment process, minimizing mistakes and saving you resources. It works best when it's fully integrated into your service and can provide you with metrics and data that will help your business grow.

Regpack is a comprehensive solution that incorporates payment processing into its other services.

Best of all, billing software isn't designed for bankers and accountants. It's developed with ordinary people in mind to make the payment process easy from both sides of the transaction.

There are many options for companies to choose from when considering billing software, which is why you should evaluate your needs and select the software that meets them best.

Regpack offers payment solutions and can make different transactions a breeze. It allows you to process payments securely and provides your clients with payment plans and recurring payment options.

Its features make it easy to build secure online payment forms, embed them on your website, and process credit card, debit card, and ACH payments.

Have you noticed that your client base is getting larger, and transactions are getting harder to track? When that happens, it's time to implement some excellent billing software to take some of the pressure off.

After all, we're talking about your hard-earned cash, which deserves to arrive safely and swiftly in your business account, with minimal margin for error.

Conclusion

We hope this article has shown you that there are many ways customers may want to pay for your excellent service. From traditional methods to high-tech solutions, each method comes with its pros and cons.

The trick to making your customers happy isn't finding the best payment option. It's allowing for as many payment methods as possible according to the transaction context.

To facilitate the payment process even more, both for you and your clients, consider using specialized billing software. That way, you're providing your clients with a better user experience and making getting paid easier than ever.