In 2021, there are many ways to move money.

When you need to accept a payment from a customer, it’s usually best to offer as many methods of doing so as possible.

ACH payments are secure and easy, making them a reliable choice for service-based companies who want to manage customer registration and payments online.

But what exactly is an ACH payment, and how do you know if it’s something you should use? In this post, we’ll walk you through the definition of ACH payments, how they work, and the pros and cons of accepting them in your business.

Jump to section:

What Is ACH?

How Does an ACH Payment Work?

Types of ACH Transfers

Wire Transfer vs. ACH Transfer

Benefits of ACH Payments

Drawbacks of ACH Payment Processing

How to Accept ACH Payments in Your Business

What Is ACH?

If you’ve ever paid your bills using autopay or received your paycheck through direct deposit, you’ve likely used the ACH network.

The Automated Clearing House (ACH) network is used to transfer money electronically, directly from one bank account to another. In the U.S., the ACH is overseen by an organization called the National Automatic Clearing House Association (NACHA).

Because ACH payments don’t require a credit card transaction, a paper check, or a wire transfer, they’re one of the simplest and easiest ways to make a payment.

And with 26.8 billion ACH transactions, 2020 was a record year for this technology, as the COVID-19 pandemic accelerated the U.S.’s shift towards electronic payments.

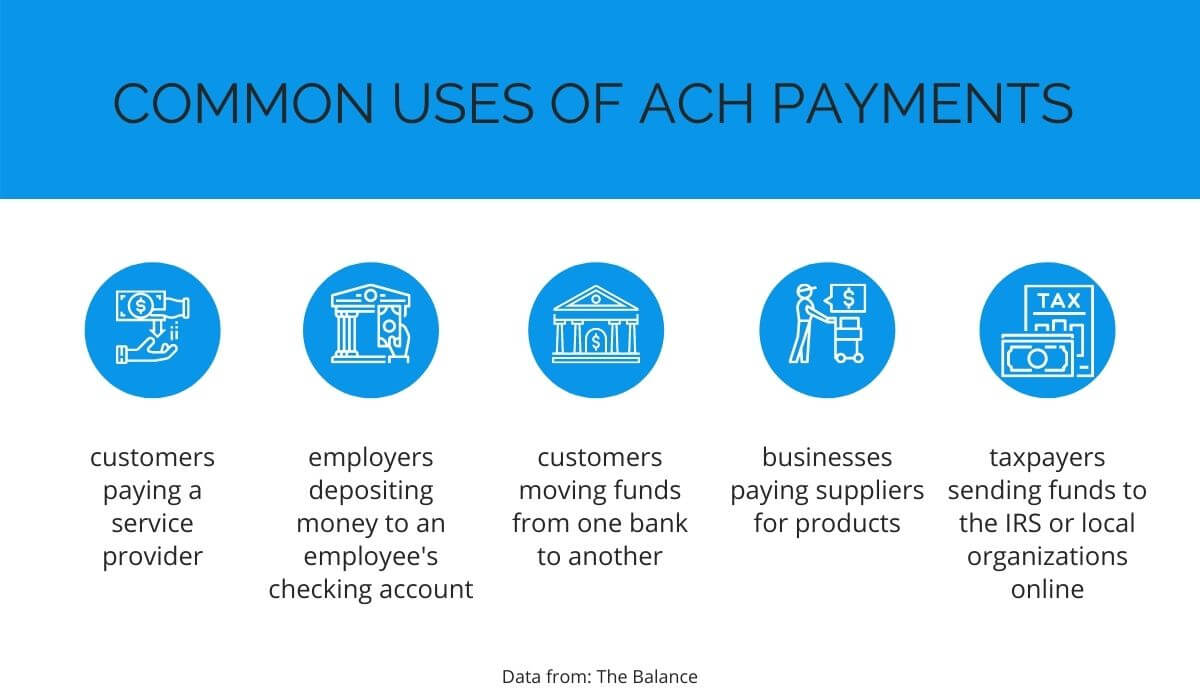

ACH transfers, also known as direct payments or electronic funds transfers (EFTs), are used for many types of transactions, including:

- Direct deposit for payroll

- Business-to-business (B2B) e-payments

- Government benefit programs

- Tax payments

- Automatic bill payments

- Person-to-person payments using third-party apps like Paypal, Venmo, and Cash App

ACH transfers are a popular method for businesses because of their simplicity and ease of use.

Source: Regpack

Instead of needing a paper check or a credit card, consumers can provide their bank account information once and let the business’s automated system take care of charging their account at the right time.

Don’t Limit Your Customer Pool!

Offer Multiple Payment Options Seamlessly

How Does an ACH Payment Work?

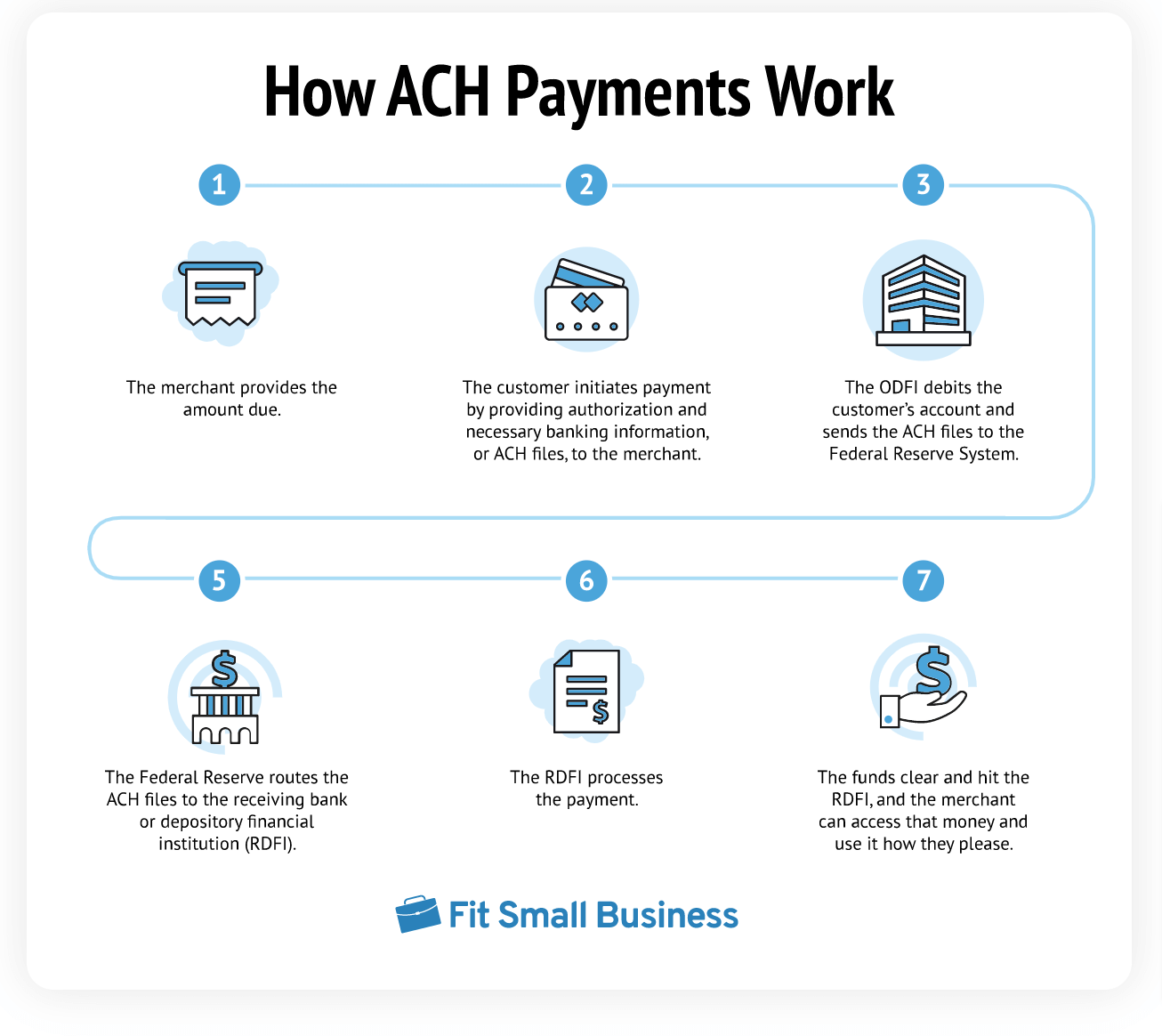

You’re probably wondering what the ACH process involves, exactly. So, let’s go over the steps.

Source: Fit Small Business

In a standard ACH payment, there are several parties involved:

- The Automated Clearing House (ACH) network, which connects all the banks in the United States

- The Originating Depository Financial Institution (ODFI), the bank that initiates the payment

- The Receiving Depository Financial Institution (RDFI), the bank that receives the funds

In a business ACH transaction, the merchant provides the invoice or bill to the customer. The customer then provides their banking information (like routing and account numbers) and authorization for ACH payments.

Then, their bank (the ODFI) debits the customer’s account and sends the charge through ACH operators to the Federal Reserve System.

The Federal Reserve System acts as an intermediary between the originating and receiving banks. It processes the ACH request and sends the files to the RDFI (the merchant’s bank).

Finally, once the RDFI processes the transfer, the funds hit the merchant’s account and the transaction is complete.

Tom Sullivan at Plaid explains how ACH payments work best:

In essence, the ACH network acts as a financial postal system. Individual transactions are like letters that ACH operators sort and deliver between various banks, where each bank is acting as a post office on behalf of their respective account holders.

Though many believe ACH payments take 3-5 days to process at baseline, this assumption is no longer completely accurate.

There are a few different processing speeds of ACH transfers, including same-day (such as direct deposits for payroll), next-day, and 2-day payments.

Settlements of payments only happen when the Federal Reserve is open, though, so ACH payment processing times are still limited to business days.

Common Example of an ACH Payment

Let’s say Acme Power is a utility company in your town. As a consumer, you have the option to sign up for autopay, which includes providing your checking account’s routing and account number and signing an authorization for recurring payments.

Once you’ve set up recurring payments, you’re ready for monthly ACH withdrawals. Each month, the ODFI (Acme Power’s bank) sends a transfer request to the RDFI (your bank) for the amount on your bill.

Your bank determines that there are sufficient funds in your account, and then it sends the money through the ACH network to Acme Power’s bank account.

Nevertheless, keep in mind that the ACH network processes these transactions in batches, so the transfer isn’t instantaneous. Your money may take a day or three to appear in Acme Power’s bank account.

How Do Global ACH Payments Work?

While ACH payments used to be limited to the United States, they are now possible internationally. However, there’s still no global system for ACH payments, so not every country will accept this type of payment.

A global ACH uses the receiving country’s clearing entity to deposit funds into a cross-border bank account. For example, while the United States has NACHA, Europe has the Single Euro Payments Area (SEPA) that includes 41 participating countries.

The process for setting up a global ACH depends on the individual banks and countries involved. Many users believe it’s best to reserve ACH payments for domestic transactions and use wire transfers for international payments.

Types of ACH Transfers

There are two main types of ACH payments: debits and credits. Both forms of payment require both the payor and the payee to give permission for the transaction; however, the difference is in which party initiates the payment.

![]()

Source: Regpack

In an ACH debit, the transfer is initiated by the person or business who isreceiving the money. The example above of a consumer authorizing their power company to withdraw the amount due on their bill each month would fall under the category of an ACH debit.

In an ACH credit, the payer initiates the transaction. The person paying the money sends instructions to their own bank to begin the payment process.

Many people use ACH credits to make a contribution to their retirement account or pay friends back after a night out. And a business that offers direct deposit payroll uses ACH credit transactions to push money into the employees’ bank accounts each pay period.

Wire Transfer vs. ACH Transfer

ACH payments aren’t the only way to move money electronically. Wire transfers have been around since the invention of the telegraph, when Western Union used its network to send money as early as the 1870s.

While both payment methods are secure and reliable, they each have pros and cons in terms of speed and cost. As Certified Financial Education Instructor Allison Martin writes for Experian:

If you’re torn between an ACH or wire transfer, consider the processing time and fees. ACH transfers take a bit longer to process, but are usually free. They’re also ideal if you’re looking for a convenient way to pay bills electronically.

Because they are processed in batches a few times per day, ACH payments typically take up to a few business days to complete.

Wire transfers, on the other hand, are completed immediately. So, if speed is your top priority, it’s usually best to go with a wire transfer.

However, the on-demand nature of wire transfers incurs higher costs. Most financial institutions charge between $10 and $35 to send a wire—and that’s just within the United States. International transfers can cost even more.

![]()

Source: The Balance

ACH and wire transfers are both extremely secure forms of payment; however, ACH transfers can be reversed. It’s much more difficult to do so with wire transfers once the transaction has gone through.

Decrease Non-Payment By 75%

With Flexible Payment Plans!

Benefits of ACH Payments

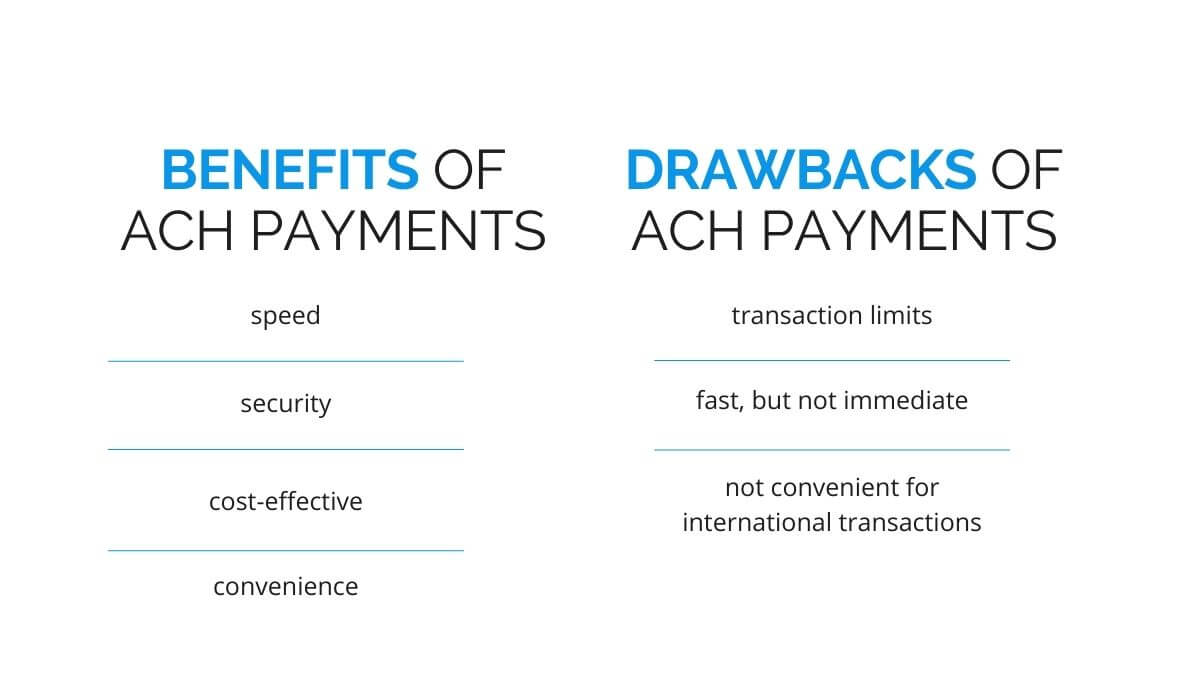

Sending online payments via ACH comes with several benefits, including speed, security, cost, and convenience.

Speed

For one thing, ACH payments are relatively quick and convenient.

They may not be as instantaneous as wire transfers (which are guaranteed to be completed within the same day, and occasionally even within the same hour), but they’re still much faster and easier than mailing a check and waiting for it to be deposited.

Security

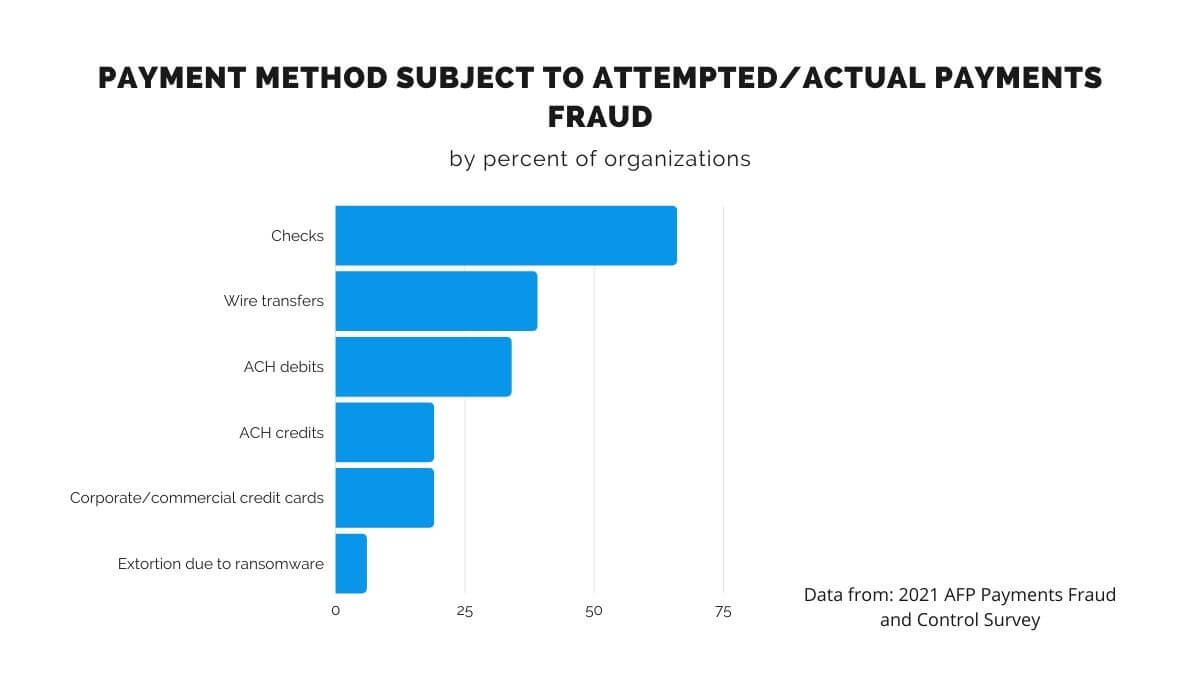

ACH payments are also a more secure form of transaction than physical payments. Paper checks can be lost in the mail or stolen.

In fact, the AFP Payments Fraud and Control Survey indicates that for businesses, paper checks are the payment method that is most subject to fraud in 2021.

Source: Regpack

Electronic transfers such as ACH use bank-level encryption—and it’s much harder to steal banking information compared to credit card numbers.

NACHA has requirements for parties involved in all ACH payments to implement protective procedures and controls. Customer information must be encrypted using “commercially reasonable” technology.

So if you use a third party for ACH payment processing, make sure to choose one with state-of-the-art encryption methods.

It’s also a good idea to check with a security expert or IT professional to make sure your company is correctly processing ACH payments on your end.

Cost-Effective

The cost of sending and receiving an ACH payment averages less than $0.75, which is negligible compared to other forms of payment like wire transfers and credit card transactions.

Wire transfers can cost anywhere from $10 to $35 and beyond—and payment processing companies charge an average of 3% per credit card transaction.

Customers using their credit cards may not care about processing fees—but businesses, especially small businesses, know that 3% of each transaction can add up fast.

Often, keeping up with the competition means you need to do everything in your power to keep prices low; and cutting processing fees out of the cost of doing business makes that possible.

Convenience

Manually making recurring payments can quickly become a headache, which is why consumers and businesses alike appreciate the ability to “set it and forget it” with autopay or direct deposit.

Customers don’t need to wait to receive a bill and keep track of payment due dates; they can simply set up automatic bill payments and kiss late fees goodbye.

And ACH payments are more convenient for merchants, too. You don’t need to worry about declined payments (or even involuntary churn) due to credit card expiration, and you’ll take fewer trips to the bank to deposit checks.

Drawbacks of ACH Payment Processing

ACH payments are a convenient form of moving money in the modern age, but that doesn’t mean they’re perfect—or right for every situation. Drawbacks to using ACH payments include transaction limits, speed limits, and a lack of international payment options.

Transaction Limits

NACHA caps ACH payments at $100,000 per transaction, though that limit will be raised to $1 million in early 2022.

This transaction ceiling may seem so high that it’ll never be a problem, but some large business-to-business companies may need to make larger transfers than that.

For most businesses, though, the dollar limit isn’t the problem.

Source: Regpack

The other limit to consider is the frequency; most savings or money market accounts limit withdrawals to six per month.

If your customer sets up an ACH withdrawal agreement through a savings or money market account and then goes over the limit, their bank may charge a withdrawal fee, reject the transfer request, or even close the savings account altogether.

Fast, But Not Immediate

While an ACH payment is much faster and more convenient than sending a check, it’s still not instantaneous. At their slowest, ACH transfers can take several days to complete.

And since ACH payments are processed in batches a few times each business day, there are cutoff times for transactions.

After a certain time, an ACH transfer won’t be processed until the following business day. Those that need to move money immediately may want to consider a wire transfer instead.

Not Convenient for International Transactions

While global ACH payments are becoming more possible, they’re still not as easy to accomplish as international wire transfers. Some banks don’t allow international ACH transactions at all.

If your business does much of its business across borders, it may be wise to offer alternative payment options to ACH for your international customers.

Accept Payments Online, Right On Your Website!

Streamline your checkout process, offer payment plans, and more!

How to Accept ACH Payments in Your Business

ACH payments are a cost-effective and convenient solution for many, but that doesn’t mean accepting ACH is right for every organization. So, should you accept ACH in your business?

Your company would probably benefit from ACH payments if one or more of the following statements apply to you:

- You take recurring payments

- Many of your customers currently pay via paper checks

- Some of your customers are uncomfortable with paying by credit card—but would consider another (safer) online payment option

- Your business is in a high-risk category that makes you ineligible to accept credit and debit card payments

If your business accepts a great deal of credit card payments, you should also compare how much you’re paying in credit card processing fees to how much you would spend in ACH fees.

Once you decide whether accepting ACH payments is right for you, you’ll need to decide on a third-party processor to run ACH payments for your business.

NACHA doesn’t allow small businesses to be the ODFI or the RDFI in an ACH transaction, so you won’t be able to accept ACH funds on your own.

Tools like Regpack securely collect payments and deposit your funds directly into your bank account as soon as possible. Regpack also provides user-friendly forms that let you set up ACH payments directly on your website.

Conclusion

In the old days, consumers and buyers had to write out and mail a check to make payments—but in our overwhelmingly digital world, that payment method is painfully old-school.

Thankfully, there’s a way for your customers to make money transfers from the comfort of their own homes. For businesses looking to manage their customers’ online payments effectively and reliably, ACH payments are a secure, cost-effective, and convenient choice.