Credit cards, cash, electronic transfers—there are so many different payment methods you could offer your customers these days that it can be hard to choose.

Generally, the best option is to offer a sprawling combination of the payment methods your customers most prefer, but that’s not always feasible or convenient for the business owner.

Sometimes, you have to be selective.

In this article, we’ll tell you the pros and cons of accepting each major payment method, from cash to mobile payments, and help you decide which ones are right for your business.

When to Choose Cash Payments

Even if online payments are gaining traction, cash is still one of the most popular forms of payment.

A 2021 study by the San Francisco Federal Reserve found that cash accounted for 19% of all payments in 2020, and that was during the pandemic, when many people stayed indoors and favored online payment methods.

Businesses that offer cash as a payment option typically accept it from a point-of-sale system at their brick-and-mortar store.

The oldest form of payment on this list, cash has stuck around for a reason.

One major advantage of accepting cash is that you receive your funds as soon as the customer makes a payment.

Most other forms of payment have financial institutions involved in processing the payment, so there are always some transaction delays. Cash evades this issue.

Businesses suffering from cash flow issues will sometimes incentivize customers to pay with cash so that they can get some operating funds ASAP.

Another benefit of allowing customers to pay with cash is that there you don’t have to pay any fees to accept the payment.

Credit cards, for example, charge a processing fee and other fees that can add up over time, even if they’re just a small percentage of the total sale.

Source: EBiz Charge

A final benefit is that some of your customers will still expect to be able to pay with cash, and offering this option to them will make them happy.

That said, while cash can be a great way to increase short-term cash flow and avoid fees, it does have its drawbacks, especially if you’re running a cash-only business.

You’ve probably had the experience of entering a small store and not being able to pay because they only take cash. Only accepting cash can cause you to lose customers.

It might also feel more painful for customers to make purchases with cash than with a card, an effect that can also hurt your sales:

Source: Get VMS

Another issue with accepting cash as payment is that it’s harder to track and manage the money that comes in. That can lead to costly accounting mistakes.

Small businesses often incur costs from accidental internal fraud, usually when an honest employee makes a mistake.

According to FAU’s study, 42% of frauds were caused by a lack of controls.

When you use online payments and the software that facilitates them, it’s much easier to set up automations and controls that almost eliminate the possibility of human error in billing and accounting.

With cash, unfortunately, it’s more difficult to ensure that your employees follow your standard operating procedures for handling money. This is its most glaring disadvantage.

In sum, cash is beneficial in that you get your money right away and don’t have to deal with fees. But it’s hard to manage and is becoming less and less the preferred payment method.

Therefore, for most small businesses, it’s probably not a good idea to go cash-only. But accepting it alongside other methods is a favorable strategy.

When to Choose Check Payments

Paper checks had their heyday in the 20th century.

They’re still a common way for grandparents to give their grandkids money, but they’re becoming less and less common as a form of business payment.

An advantage of accepting paper checks is that some of your customers who like to pay with checks will appreciate it.

This preference for paper checks is most common among people without credit or debit cards or during a recession. Plus, there aren’t any set-up fees or costly software involved.

However, a serious problem with accepting them is that the check has a risk of bouncing if the customer has insufficient funds in their account.

If that happens, you might have to go through a costly small claims court process to get your money.

Customers can also stop payment of a check at any time after they’ve already left your store with the purchased merchandise. Not to mention, you could lose the check in transit.

These days, electronic checks, or ACH transfers, are typically a better option for small businesses than physical checks.

E-checks are more convenient to pay, as they can be filled out and submitted from anywhere as long as the payee has access to the internet and their bank’s routing number.

They do incur a small fee to the business owner, but it’s usually smaller than credit card fees.

Plus, e-checks process more quickly than physical checks, for the following reasons:

| You don’t have to walk to the bank to deposit the check. |

| Paper checks require longer hold times than e-checks. |

| E-check processing happens digitally, which is almost always faster. |

Ultimately, compromising and accepting e-checks and doing away with paper checks is the best and safest option for most small businesses.

When to Choose Card Payments

All small businesses should accept at least one type of card payment, debit or credit, and preferably both.

You want to give your customers the ability to pay with their preferred method, and cards are typically that.

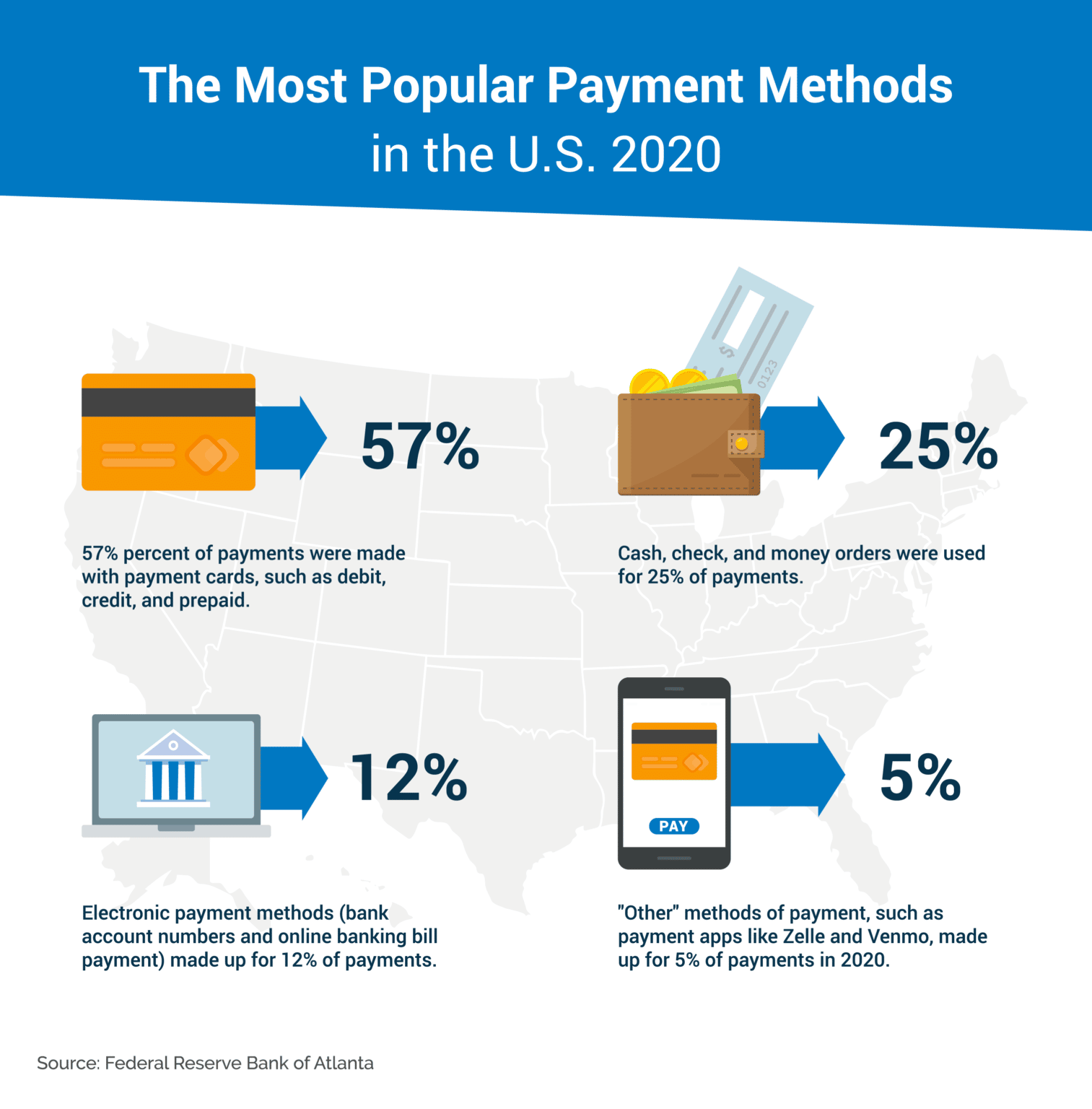

Paying with cards is the most popular method in the US:

Source: Upgraded Points

Not offering credit or debit card payments would be like not offering vanilla and chocolate ice cream at a new ice cream shop. It just wouldn’t go over well. You’d get some funny looks.

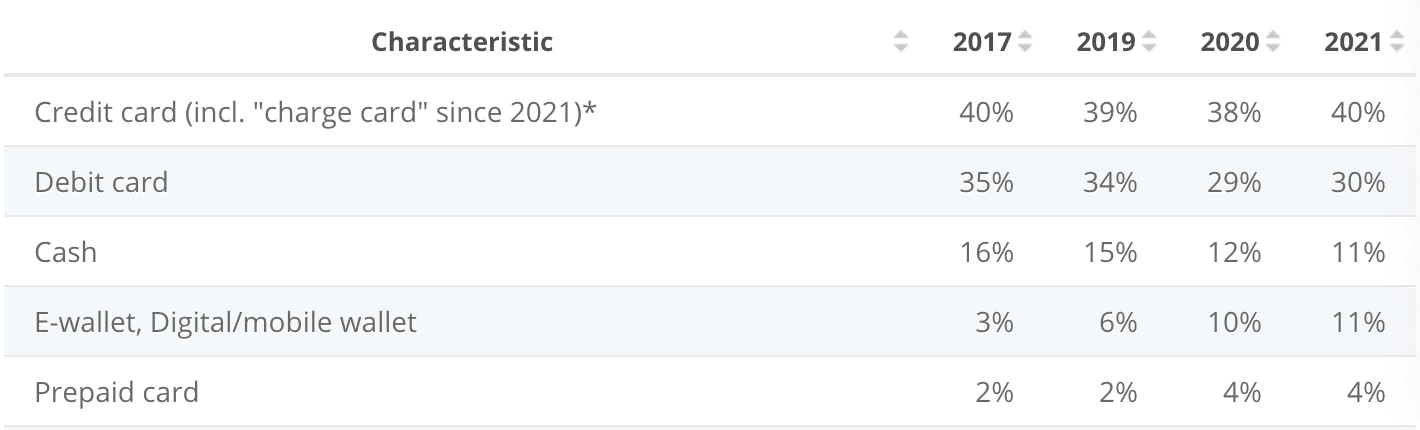

According to Statista, credit and debit card payments accounted for 70% of all payments at point-of-sale systems during 2021:

Source: Statista

Customers prefer using their cards to pay for a couple of reasons. First, it allows them to finance large purchases.

So if your business is selling high-ticket items, credit card acceptance is a near necessity.

Second, the whole checkout process is incredibly smooth, whether they’re doing it online or in person at your store.

Many customers also have their card data saved on their phone, which allows them to make online purchases with a tap of a button.

Accepting card payments benefits your business in other ways than pleasing your customers and expanding your potential customer base.

Card payments usually have short transaction periods, so you’ll get your funds within a few days, which is great for cash flow.

It’s also a secure form of payment and makes your business appear more credible and established to customers and investors.

That said, with all its benefits, there are some drawbacks to accepting credit and debit card payments.

Here are the biggest ones:

| Potential for chargebacks | When customers dispute charges, your account will be debited without warning. |

| Fees add up | Card companies make you pay transaction fees, flat fees, and other fees that negatively impact your revenue. |

| Monthly minimums | Sometimes you need to accept a certain number of transactions via card or else you’ll have to pay a fee. |

| Compliance costs | You’ll need to ensure you’re PCI DSS compliant. Sometimes that requires time and money. |

Despite the complications that come with accepting credit and debit cards, it’s still crucial that your business accepts at least one, or else you’ll miss out on a large portion of potential customers.

When to Choose Mobile Payments

Small businesses can accept contactless payments from customers who have a mobile device (like a smartphone or smartwatch) with near-field communication capabilities (NFC).

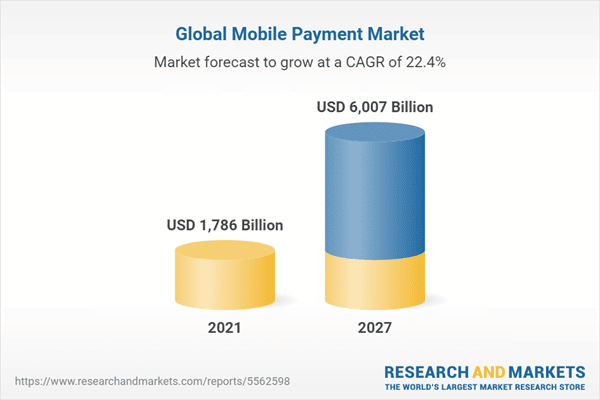

This payment method is gaining traction, with 1.7 billion dollars worth of transactions occurring via mobile payment in 2021.

That’s a 27% increase in usage from 2020. And usage is expected to grow quite dramatically over the next five years:

Source: Research and Markets

Some consumers love this form of payment because it means they don’t have to carry around a wallet or purse.

Therefore, the most significant benefit to businesses of accepting this method is pleasing this type of customer.

Whenever your business is able to streamline the payment process for your customers, you improve the customer experience and receive the increased sales and loyalty that follows.

With mobile payments, all your customers have to do to complete the purchase is tap the screen of their mobile device. Payment doesn’t get much easier than that.

On the other end of the spectrum, offering mobile payments can be both technologically tedious and expensive for smaller businesses.

You’ll have to invest in special payment terminals that are capable of accepting mobile payments.

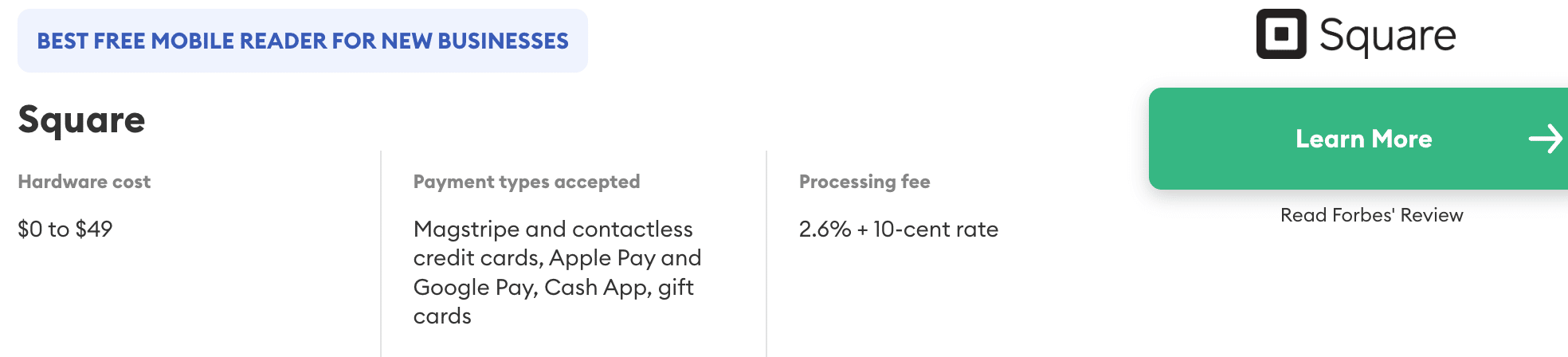

These come with upfront hardware costs and ongoing processing fees that range from 2.26% to 2.6% in addition to 10 cents per transaction.

Square, a mobile reader, is on the more expensive side for processing fees, but it’s still a reliable option for new businesses, and its hardware cost can be free:

Source: Forbes

Also, you should expect to pay transaction fees for payments made with a mobile device because the customer is often drawing the funds from a credit or debit card, both of which come with fees for the merchant.

Further, compliance can be tricky because each mobile payment app (Cash App, Samsung Pay, etc.) has its own set of rules regarding customer protection.

So, you’re going to have to comprehend and comply with a large number of policies if you accept a wide range of mobile payment types.

In sum, whether or not you choose to accept mobile payments should come down to how many of your customers want to use this method at your business.

It’s most popular in the retail, food, and entertainment industries.

If a large chunk of your customers prefers them, it might be a good choice to include mobile payments in your payment mix.

If not, it’s okay to put this on the back burner and focus on implementing a more popular method of payment, like credit or debit cards.

When to Choose Online Payments

Online payments enable customers to make payments on their computer, tablet, or mobile device, often through a user portal or website. They’re fast, convenient, and secure.

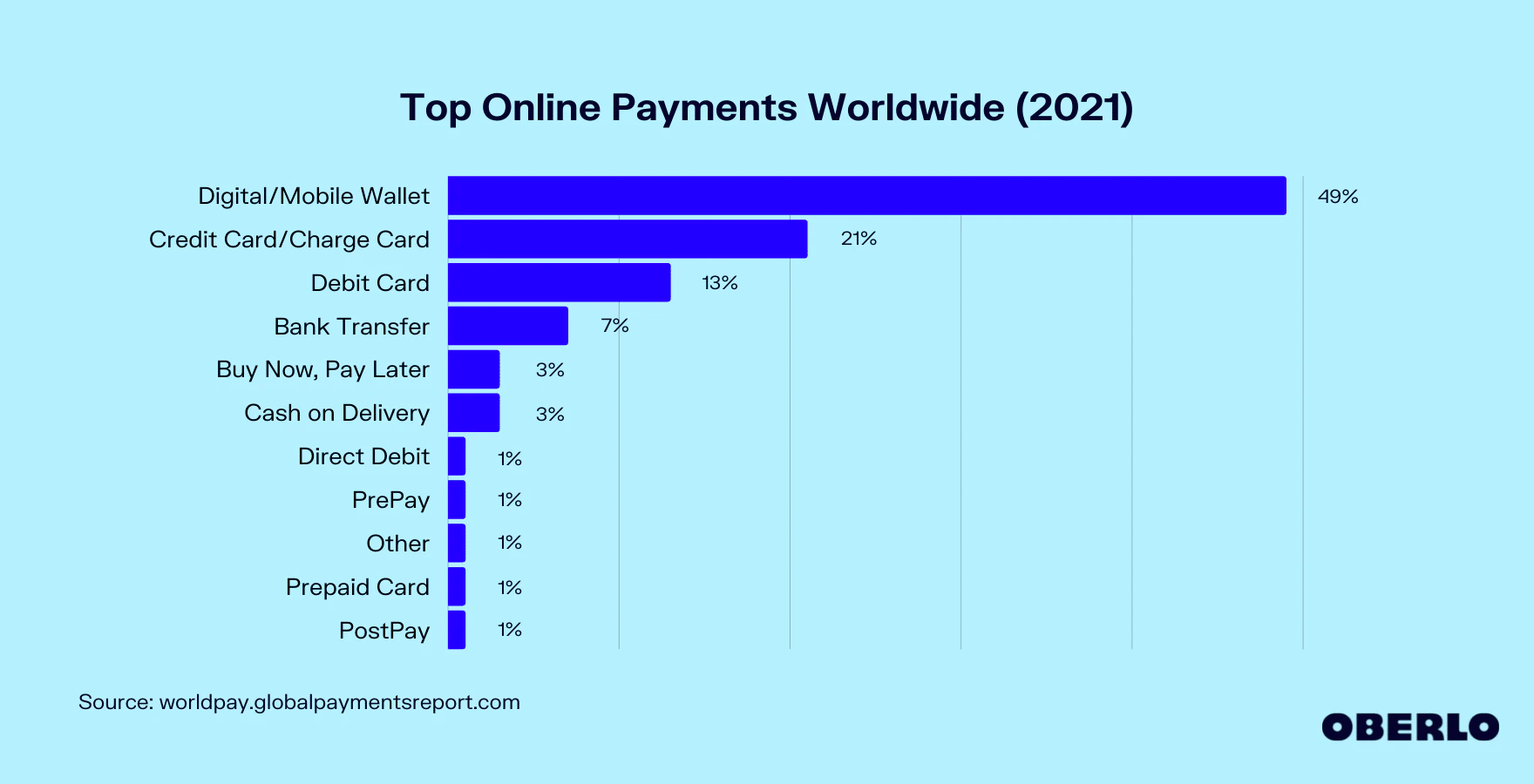

Major types of online payment methods include credit and debit cards, ACH transfers, mobile wallets, and other ones that allow for funds to be transferred electronically:

Source: Oberlo

Online payments are becoming increasingly popular, so businesses should give online payment methods serious consideration.

Statista predicts that the total worldwide transaction value of digital payments will rise from $8.49 trillion in 2022 to $15.17 trillion in 2027.

They’re also one of the most popular B2B payment methods.

For small businesses, one of the major advantages of accepting online payments is that they automate and speed up the payment process.

You don’t have to have someone on your team interact with the customer while they pay. Customers can self-serve and make payments in an online form without any assistance.

If it’s convenient for you, it’s just as convenient for the customer.

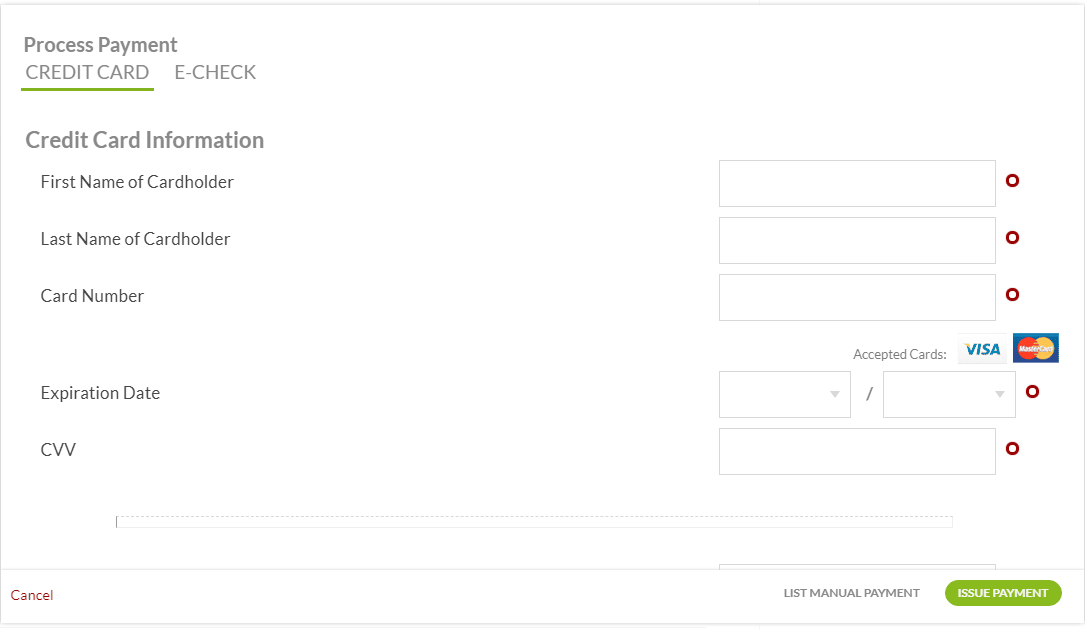

They can pay for your products or services from the comfort of their couch in a matter of seconds through an online form, as shown below:

Source: Regpack

We have an entire article going in-depth on five reasons small businesses should accept online payments.

One of the reasons we mention is that these payments are secure, provided that the online payments software you’re using is following protocols around data protection.

Consequently, one of the trickiest parts of accepting online payments is finding the right online payment platform to process these payments. Here are some tips for choosing wisely.

First off, your provider should be PCI DSS compliant and focused on protecting the financial data of you and your customers.

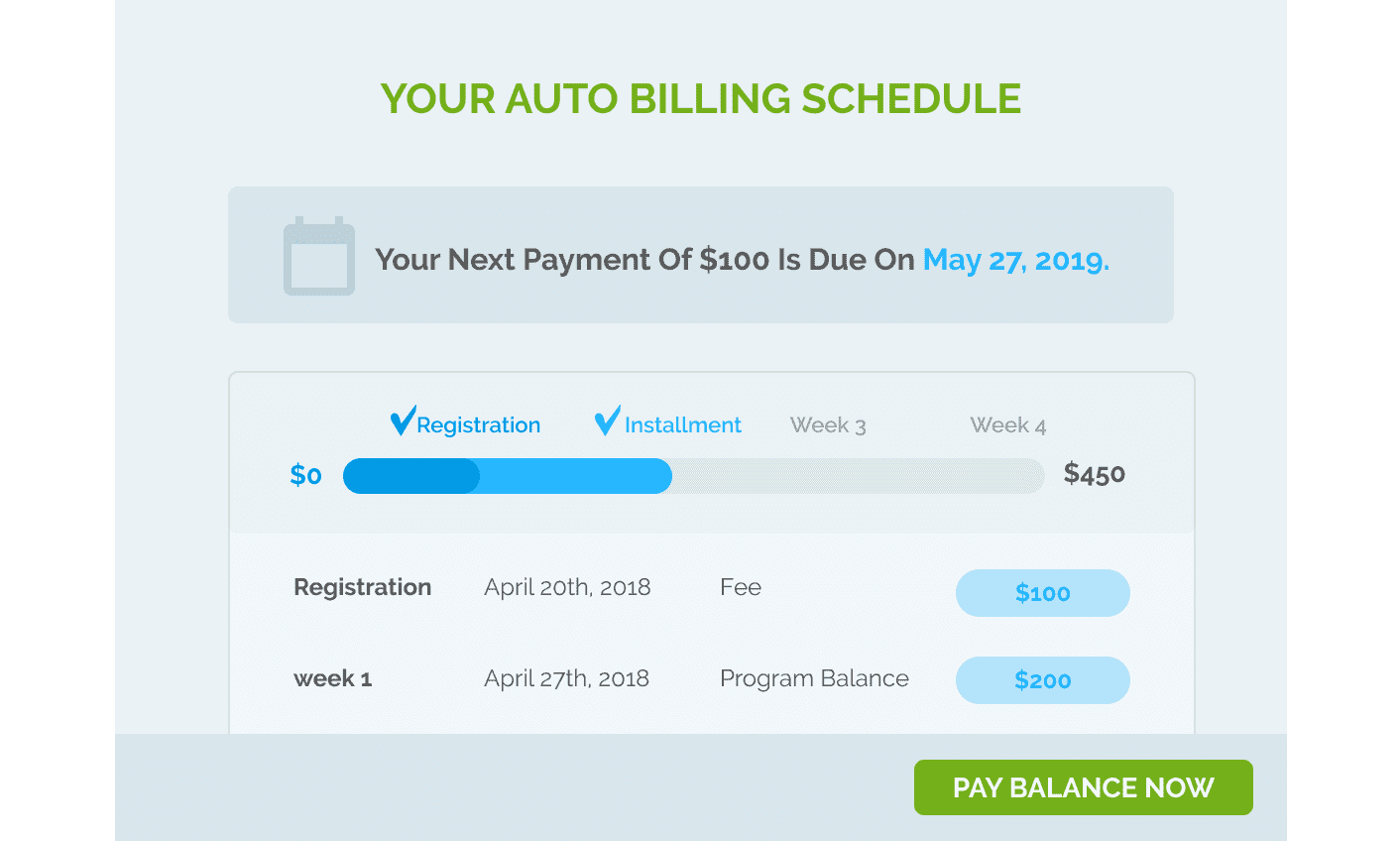

Second, the software should come with features like personalized payment plans and user portals that tremendously improve the payment experience for your customers:

Source: Regpack

Third, it’s crucial that your provider facilitates payments with the payment methods you’d like to offer. Some might allow for mobile wallet or ACH transfer payments, while others will not.

Fourth, online payment software providers often design their platform to serve a specific type of customer. So look for one that helps businesses like yours.

For example, Regpack is an online payment software that helps primarily small service-based businesses. So they have features that reflect that target customer.

Source: Regpack

In sum, online payments are a great option for small businesses that want to save time, automate the payment process, reduce human error, and satisfy their customers.

Conclusion

There are a lot of decisions you have to make when running a small business — a lot of research and weighing of options to do.

Hopefully, we made the process of selecting the right payment methods a little easier for you today.

As a final note, the best payment strategy is often a mixture of different payment methods.

By playing wide, you can ensure that a higher number of your customers are able to use their preferred method.

If you need any guidance, feel free to reach out to the Regpack team.