There’s some confusion around the difference between a merchant account and a bank account.

Small business owners need to know what purpose each one serves, their key characteristics, and how opening them will affect their business.

In short, if you want to collect credit card, debit card, and other online payments from customers, you’re going to need to open up both types of accounts.

By reading this article, you’ll gain a foundational understanding of the basics of both accounts. You’ll also know how they differ, and how they can benefit your small business.

That way, when you shop around for the best accounts, you’ll be well informed.

- What Is a Merchant Account

- What Is a Business Bank Account

- Merchant Account vs. Business Bank Account: Key Differences

- When Do You Need a Merchant Account

- When Do You Need a Business Bank Account

- Conclusion

What Is a Merchant Account

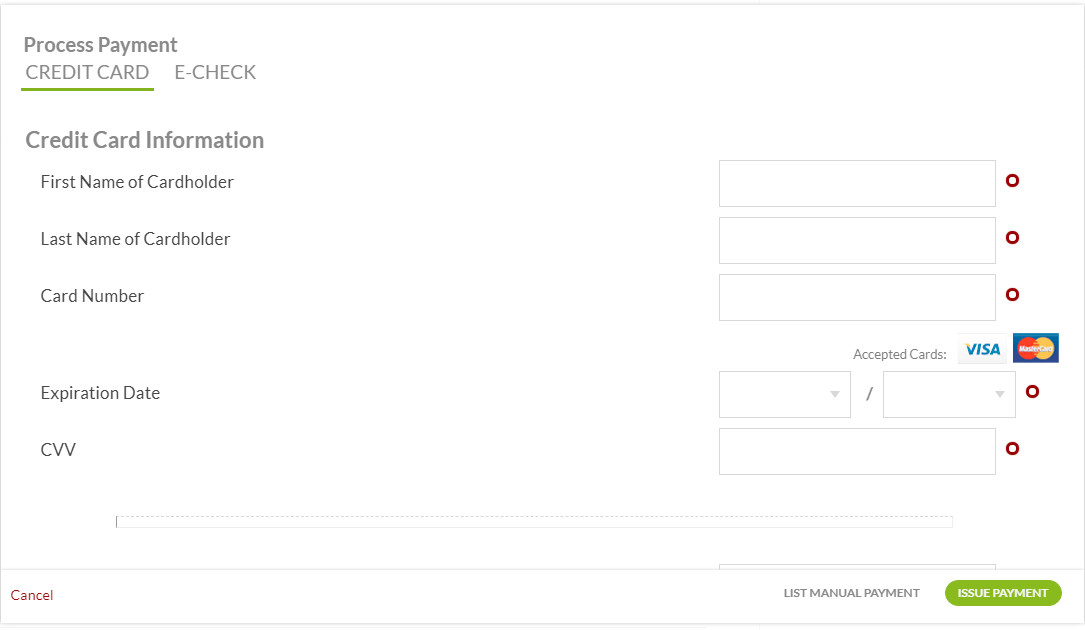

A merchant account is a type of business bank account that enables businesses to accept credit and debit card payments, as well as online payments.

It’s essential for businesses that want to offer cashless payments to their customers.

Online businesses collect the information for these cashless forms of payment through payment gateways, such as the one below:

Source: Regpack

Physical businesses will use a card terminal, like the credit card machines you see at convenience stores:

Source: Paymentix

When customers insert their card or type the card information into a payment gateway on a company’s website or app, the information is sent to the merchant bank — the bank providing your merchant account.

This bank then facilitates communication between various parties involved in processing the cashless payment and ensures the proper transfer of funds from the customer’s account to yours.

First, the acquiring bank sends the transaction information to the customer’s card issuer, also known as the card provider, who checks if they have sufficient funds to make the payment.

These are companies like American Express, Chase, and Discover.

The card issuer either approves or denies the transaction, and then sends their answer, in data format, back to the electronic terminal where the customer paid.

If it’s denied, the customer will see an alert on the electronic terminal.

If the issuer approves the transaction, the payment is processed and transferred into your merchant account, where it will be held for an average of 24-48 hours before it moves into your business bank account and is available for use.

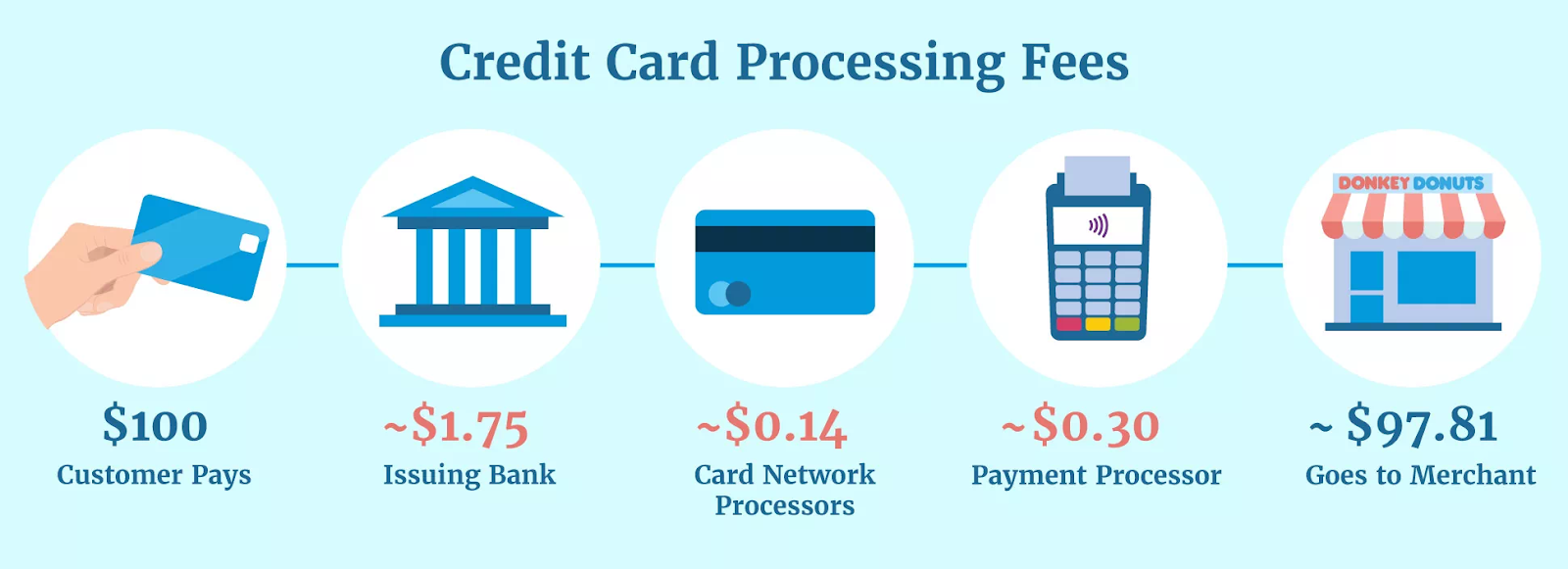

This all occurs in a matter of seconds and incurs various fees for the merchant account owner that vary based on their provider.

The most expensive fee will be the per-transaction fee charged by the acquiring bank.

Source: Credit Donkey

These fees usually run anywhere from 1.75% to 3% of each transaction’s dollar amount, plus 20 to 30 cents per transaction.

For example, the popular merchant account provider Square has a rack rate fee of 2.6% + 10 cents for contactless payments, chip cards (either swiped or inserted), and swiped magstripe cards.

They, and other banks, charge a bit more for virtual payments—3.5% + 15 cents per transaction.

That’s because these online, contactless payments are more vulnerable to card fraud.

Another reason is that the bank also doesn’t get to make money off you by leasing you a card terminal.

What Is a Business Bank Account

A business bank account allows for business transactions and is a legal requirement for all businesses except for sole proprietors.

It is where funds from a merchant account end up, as well as cash and check deposits from your customers.

The funds in the business bank account are typically used for regular business expenses, such as monthly electricity bills, software subscriptions, or payroll processing costs.

There are, however, some unique characteristics of a business bank account that you should know before you open one up.

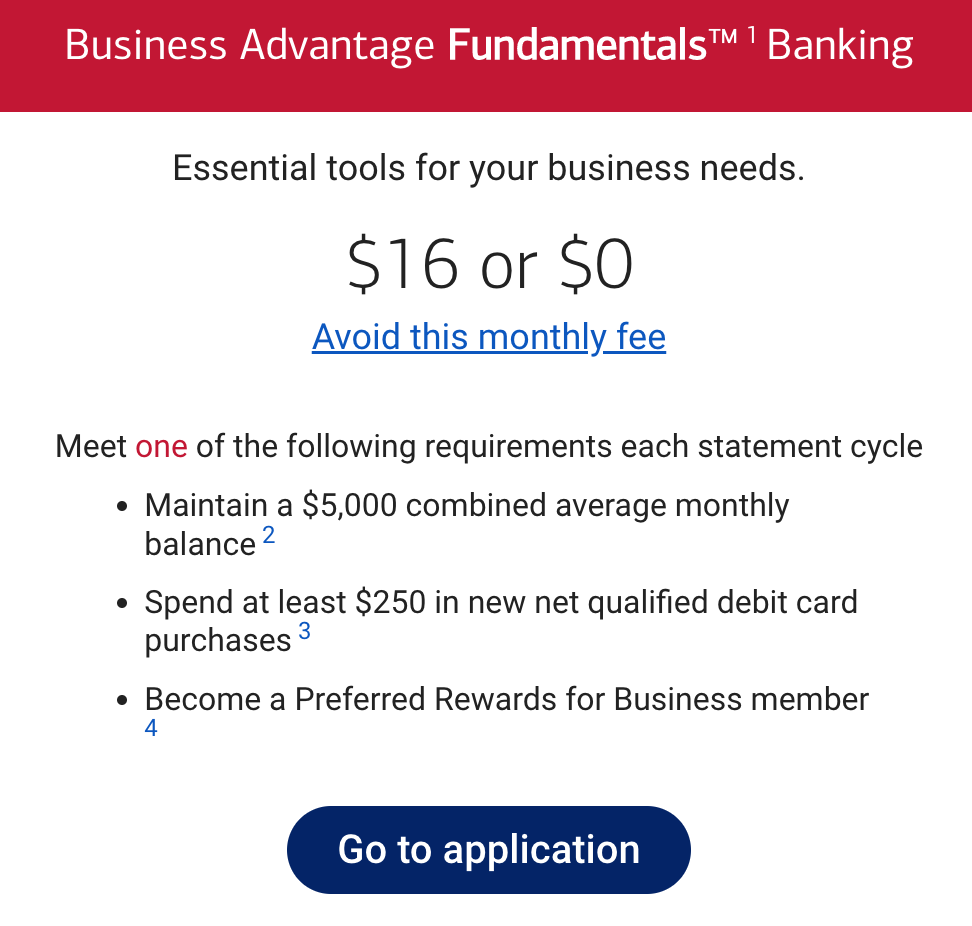

First off, most banks charge a monthly or yearly maintenance fee to keep your account open. The size of this fee depends on the bank.

And there are ways to get the bank to waive it.

For example, Bank of America usually charges $16 per month for their business bank account.

However, they erase it if you meet one of the below requirements each statement cycle:

Source: Bank of America

Bank of America rewards its clients for maintaining a high balance, but many banks may take on a different, hitting you with fees for going below their balance minimum.

Another factor to take into account is the transaction limit.

Some banks will put a cap on the number of free transactions you can process over a specified time frame—typically around 200 per month.

Check out this article to learn more about potential fees.

Typically, the more funds you have in the account, the more transactions you can make. Banks tend to give customers rewards for entrusting them with lots of money.

Lastly, business bank accounts also usually come with useful reporting tools that will help you with taxes, cash flow management, and expense tracking.

Merchant Account vs. Business Bank Account: Key Differences

Businesses use a merchant account and a business account together to process and accept credit card, debit card, and online payments from customers.

However, the two types of bank accounts have some major differences.

In terms of accepting card payments, the main difference between a merchant account and a business account is that credit card payments made to a merchant account will process much faster than those made to a business bank account.

When a business bank account accepts a card payment, the acquiring bank and the issuer will delay the payment until they both authorize the transaction.

This takes at least a few days, which can hurt cash flow.

The merchant account, on the other hand, bypasses this delay, fronting the merchant the money even though online transactions may still be pending.

That’s possible for two reasons. First, they have special relationships with card providers.

Second, these banks are prepared to take on the risk of fraud—business bank accounts are not.

A merchant account’s business model is built around managing risk.

They vet the merchant through an application process, whereas the business bank account just has them fill out a few forms.

They also anticipate losing some money to fraudulent purchases and are prepared to handle that loss.

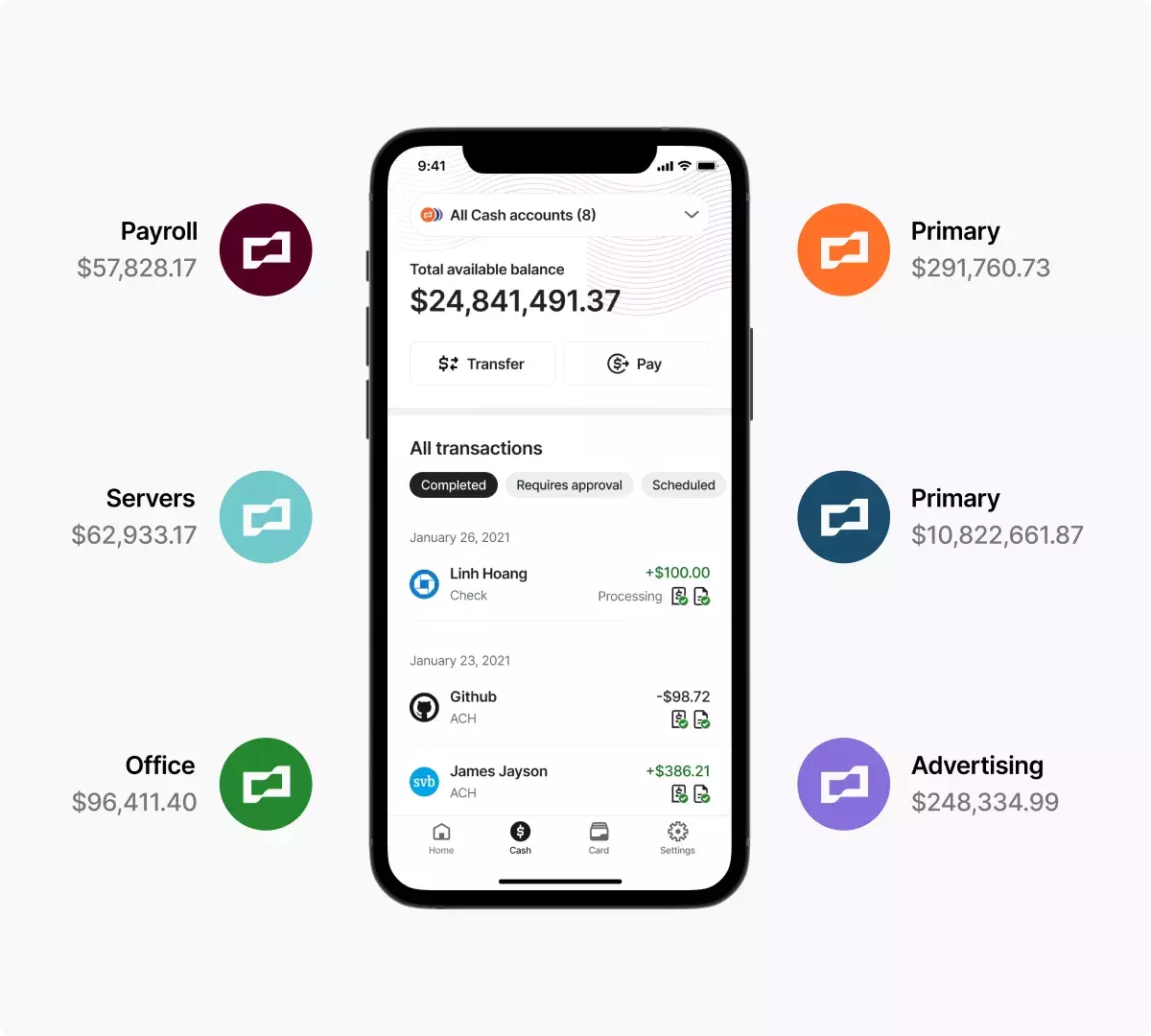

Another key difference is that business bank accounts allow for funds to be directly withdrawn from and deposited into the account. This is not possible in a merchant account.

So, business bank accounts are primarily used for tracking and paying day-to-day business expenses, like office rent, payroll, or advertising:

Source: Brex

On the other hand, the merchant account is where you manage your credit and debit card transactions.

After a credit card purchase from a customer has been approved, the money will go into your merchant account.

From there, you can transfer the funds into your business bank account, where you can then use it to make purchases, pay bills, and run your business.

Transfer times depend on the bank, but they’re usually around 1-2 days.

When Do You Need a Merchant Account

Merchant accounts are necessary for businesses that want to accept credit, debit, and other online payments from their customers, without having to wait days for the acquiring bank and issuer to individually authorize each transaction.

Allowing customers to pay through cashless and online means is becoming increasingly important in this economy, so more and more businesses are opening merchant accounts.

If you’re an online business, a merchant account is especially important, since collecting cash is not really a viable option.

Customers would have to send it over mail, a long and risky process.

Instead, with a merchant account, businesses can set up online payment gateways where customers can make online, cashless purchases without even interacting with a staff member, right from their laptop or phone.

Physical businesses need merchant accounts as well. It’s rare that a business only accepts cash. Customers are often confused when they encounter one that says no to credit or debit.

Even mobile businesses like taco trucks are accepting credit and debit cards these days. They simply use portable card terminals provided by their merchant account provider.

Some, like Square’s, can even attach to their smartphones:

Source: Square

That said, know that you also need to set up a business bank account before you apply for a merchant account.

Acquiring banks (merchant account providers) require businesses to deposit their funds from the merchant account into a business bank account, rather than into a personal checking account or something else.

A merchant account offers many other benefits to small businesses.

You can accept payments in different currencies, streamline cash flow, and demonstrate the legitimacy of your business, hence building authority in your niche.

Not to mention, when you’re accepting cashless payments, it’s likely that your sales numbers will increase.

No longer will customers leave for some other business because their preferred payment option isn’t available.

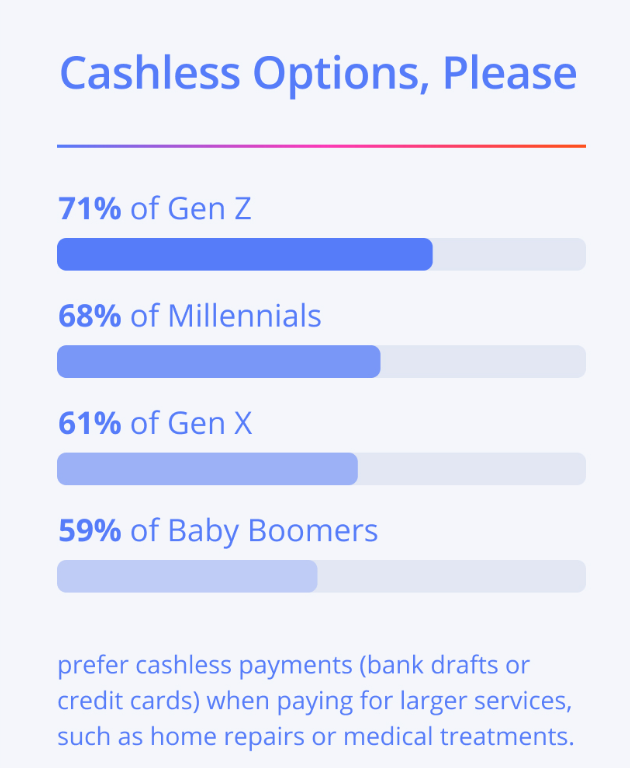

This is especially true for those selling larger services:

Source: Thryv

As each generation leans into cashless payment, it’s important to set your business up with a merchant account to easily process credit cards, debit cards, and other forms of online payments.

When Do You Need a Business Bank Account

If you want to open up a merchant account to collect cashless payments, you need to have a business bank account.

Even if you don’t want to offer cards as a payment option, your business is likely required by law to have a business bank account, unless you’re a sole proprietor.

If you run a corporation, a Limited Liability Partnership (LLP), or a Limited Liability Company (LLC), a business bank account is the way to go.

Even sole proprietors should consider opening business bank accounts, as they provide an extra level of legal protection from lawsuits.

That’s because if you keep your personal and business finances separate, your personal assets won’t be touched.

Only the funds in the bank account are at risk of seizure. This is one of many reasons to keep your business finances separate:

Source: Connecteam

Another benefit of having a business bank account is that it makes your company look more professional and credible to customers.

When you’re able to accept credit and debit cards, buyers trust that you are up to speed with the latest trends.

Using a business bank account also makes it easier to manage tax preparation. Many businesses pay quarterly business taxes.

Having all your expenses and income captured in one online place makes it easier to estimate these quarterly tax payments.

On the other hand, if a sole proprietor is using a personal bank account as the holding place for customer payments, it might be hard to tell which income came from business sales and which came from a Venmo from a friend or another source disconnected from the business.

It’s also important to note that if your business is selected for audit and you don’t maintain a business bank account, the auditor may be able to look through your personal account.

Another benefit that might not get enough attention is how opening a business bank account lays the groundwork for a good relationship with a bank, which can help you secure business loans and other forms of funding down the line.

It’s a much better experience to navigate these sometimes tricky financial situations with a bank that you trust and enjoy working with.

To open a business bank account and start reaping these benefits, there aren’t too many steps to follow:

Source: Patriot Software

Some banks even let you open an account online.

The part that should take the most time, as it’s the most important to get right, is choosing the best bank for your business’s specific needs.

Here’s a guide from Forbes Advisor on how to choose the right bank for your business bank account.

Conclusion

According to Statista, credit and debit cards are the most popular forms of payment in 2021.

It’s, therefore, essential that you set your business up to accept these cashless methods from your customers. They’ll surely appreciate it.

To do so, small businesses need to open a merchant account and a business bank account.

Both are necessary for accepting these payments, as well as other online, contactless methods, without experiencing any long delays.